1. South Pacific

2. East Asia

3. Europe

4. Latin America and the Caribbean

5. North America

6. Near East and North Africa

7. South and Southeast Asia

8. Sub-Saharan Africa

1 This review is based on the regional study prepared by the FAO interdepartmental task force, headed by D. Doulman, Fishery Policy and Planning Division/International Institutions and Liaison Service (FIPL). The information is based on written contributions by Dr Tim Adams of the Resource Assessment Management Section, Coastal Fisheries Programme of the South Pacific Commission, Noumea, New Caledonia.

The region covers the western and central Pacific Ocean, stretching from Australia in the west to Pitcairn Island in the east. There are 16 independent states as well as dependent territories of France, the United Kingdom and the United States. Two of the states, Australia and New Zealand, are developed while the remaining states and territories are small island developing states (SIDS). The main fishing areas are the southwest and central Pacific Ocean and the eastern Indian Ocean.

Although the South Pacific region provides only about 2 percent2 of total world fishery production, the fisheries sector - together with tourism - plays a critical role in the economies of the South Pacific states and territories. The region’s inshore and offshore fisheries resources are harvested for food, for sale on national markets and, above all, for export. The South Pacific has one of the world’s richest tuna fishing grounds, and fisheries exports from the region consist almost wholly of tuna. Food fish consumption is relatively high in the region at an average of 20 kg per caput annually (live weight equivalent). Excluding Australia and New Zealand, the average for some small island developing states alone would probably be twice as high.3

2 Including fishing by foreign fleets.RESOURCES AND PRODUCTION3 Precise statistics on fish supplies in the Pacific islands are not available.

Marine fisheries

The total domestic marine fishery production of the region was 769 000 tonnes in 1994, making up almost 90 percent of total fish production. Almost another 1 million tonnes of tuna is harvested annually by foreign fleets. In the 1980s and early 1990s, regional production rose much more quickly than the global average, but has declined in recent years mainly as a result of restructuring in Australian commercial fisheries and changing management regimes in New Zealand (see below). The bulk of aggregate landings originate from the fishing area of the southwestern Pacific Ocean, mainly caught by New Zealand. Australia also fishes in the eastern Indian Ocean and the catch of the small island developing states (SIDS) is mainly harvested in the western central Pacific Ocean.

In the SIDS, the main types of fisheries are distinguished by their pattern of operation and the way they are administrated. For industrial fisheries, tuna is the main target and distant-water fishing fleets from several countries outside the region participate through access agreements; in fact, Pacific island national fleets take only about 6.5 percent of the total catch of around 1 million tonnes. Small-scale coastal fisheries are divided between those targeting export products and those fishing for domestic consumption. Export production includes high-value products for specific niche markets, for example sea cucumbers, snapper and mother-of-pearl shells. There is very little interaction between the export fisheries and domestic fish production, and the species exported are usually not part of the traditional local diets. However, the species exported are also retained for the local tourist industry. The species consumed locally include crustaceans, reef fish and pelagics such as tuna and swordfish.

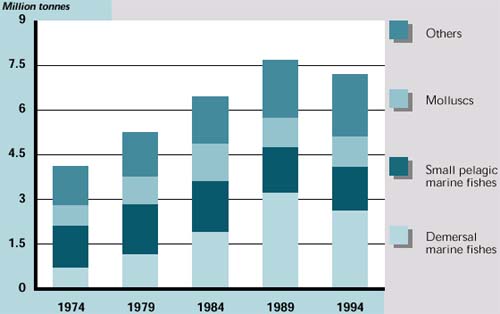

Figure 30. Regional fish production and share of world production in percentage

Throughout the Pacific islands, little is generally known about the volumes of coastal fish catches and the status of stocks: export categorization is often confused; coastal fishery stock assessment is virtually non-existent; and most of the information used in policy-making is anecdotal in origin. SIDS are concerned about the impact of high-seas fishing by foreign fleets in the region; about 20 percent of the South Pacific region is covered by high seas that fall between the exclusive economic zones (EEZs) of island states and territories.

In the Pacific island states and territories, industrial fisheries technology has tended to be of an intermediate level. A lack of trained work force and of the infrastructure necessary to support sophisticated industrial fishing operations is characteristic in most states and territories in the region. Foreign fishing fleets operating in the South Pacific are monitored by the Forum Fisheries Agency and a number of activities relating to conservation and management have been put in place for these fleets, including a regional cap on the number of purse-seine vessels permitted to operate. In coastal fisheries there are localized excess capacity problems particularly around atolls and reefs. The main challenge for states and territories in the region is to achieve sustainable resource use while ensuring the greatest socioeconomic benefit.

As would be expected of developed states, fishery technology and infrastructure in Australia and New Zealand are advanced and appropriate to a modern fisheries industry. In the trawl fisheries, these two states lead the world in deep-water trawling technology. In nearshore fisheries, harvesting methods and small vessel design also use extremely high technology - in many cases this is assisted by the extensive small boat leisure industry, which requires similar technologies and services. Australian catches include a large variety of species - scallops, lobster and orange roughy being among the more important. New Zealand catches have recently been dominated by blue grenadier, as well as squid, jack and horse mackerels and orange roughy. Several stocks have shown signs of overfishing recently. In both countries, the management of excess capacity is not a particularly contentious issue. Fleets have been reduced, particularly the prawn fleet in Australia’s Gulf of Carpentaria which, through rigorous industrial management, has decreased from 292 vessels in 1977 to 125 vessels in 1993.

Inland water fisheries

Owing to the good supplies of freshwater, significant inland fisheries are restricted to the larger land masses of the region (i.e. Australia, New Zealand and Papua New Guinea). In Australia and New Zealand, inland fisheries are valued as a recreational resource and not as a source of food security. On the other hand, in the highland areas of Papua New Guinea inland fisheries are very important owing to restricted access to marine coastal areas and limited production of other sources of animal protein. Some SIDS also support a certain level of inland water fishing as well as specialized fisheries. The total inland capture fishery harvest in the South Pacific region in 1994 was 25 102 tonnes. River eels, barramundi, freshwater molluscs and crustaceans, tilapia, gudgeons and sleepers are found in the region. Salmonids, such as rainbow and brown trout, are common inland sport fish in Australia and New Zealand.

Data for inland fisheries do not include sport and recreational fisheries, which are important in developed areas such as Australia and New Zealand. Although data on recreational fishing throughout Australia are limited, anglers now appear to be the dominant harvesters of several estuarine fish species. The growing number of recreational anglers in Australia, and probably elsewhere, could lead to both heightened conflict among user groups and greater exploitation of the limited resources.

Figure 31. Fish utilization and food supply

Figure 32. Fishery imports and exports (including intraregional trade)

N.B. FAO trade statistics available only from 1976.Aquaculture

Aquaculture production has risen from some 20 000 tonnes in 1984 to almost 75 000 tonnes in 1994, mainly owing to increases in New Zealand and Australia. Excluding the two major producers, the remaining Pacific states and territories contributed a mere 2 500 tonnes in 1994. The major increase from a single species was from mussel cultivation in New Zealand, which grew from 9 800 tonnes in 1984 to 47 000 tonnes in 1994. Other significant, rapid increases have been observed in the culture of salmon in New Zealand and of Salmo salar in Australia. Oysters and pearl oysters are other important species. Most aquaculture production is derived from coastal aquaculture, even though the physical potential for freshwater aquaculture development could be considerable in larger countries.

PRODUCTS AND MARKETS

Apart from in Australia and New Zealand, fish is a culturally and nutritionally important source of food throughout the region. The diet of the Pacific islanders depends heavily on fish and most states and territories derive a high proportion of their animal protein supplies from fish, ranging up to a high of 69 percent for Kiribati and with almost all states deriving over 25 percent from this source. Actual fish consumption is difficult to estimate, however, because of the limited statistics available and the unknown contribution from unrecorded household catches. The figures for per caput food fish supply provided by FAO probably underestimate overall consumption. These figures have shown a steady upward trend over the years and range up to 100 kg per head per year (live weight equivalent) for Tokelau. The regional average as a whole was 20 kg per person in 1994, but the average for the island countries alone - excluding Australia and New Zealand - is at least twice as high.

Fisheries exports from the region consist almost wholly of tuna, which is the South Pacific’s most important development resource. Canneries in American Samoa, Fiji and the Solomon Islands export tuna at slightly higher prices than their Southeast Asian counterparts, but the latter two states benefit from African, Caribbean and Pacific (ACP) status in the European Union (EU) market.4 Exports of fishery products from Australia and New Zealand are encouraged by sophisticated fish-processing industries geared to exporting high-value products to discriminating markets.

4 The EU has a trade agreement with 69 countries in Africa, the Caribbean and the Pacific. However, with the new General Agreement on Tariffs and Trade/World Trade Organization (GATT/WTO) agreement, these privileges will be withdrawn gradually. See Box 22 on p. 103.Figure 33. Fishery production by species categories

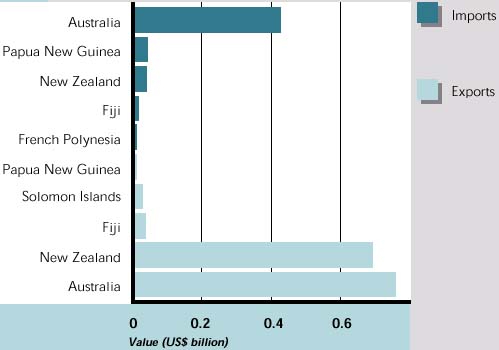

Figure 34. Fishery imports and exports for major trading countries in 1994

FISHERIES POLICY AND MANAGEMENT

Most national fisheries administrations in the Pacific islands are small and fragile with only a limited range of technical expertise. High priorities are assigned by governments to policies aimed at institutional strengthening and capacity building because of the importance of fisheries among these countries. In the early 1990s, action was taken to restructure the national fisheries administrations in Australia, New Zealand and Papua New Guinea. In each case, national fisheries authorities with semi-commercial status were established and these have facilitated a more prominent participatory role for the private sector in fisheries administration, including private-sector financial contributions to the costs of administration and research.

The socio-economic development of many South Pacific island states and territories is closely tied to the fortunes of regional fisheries. Hence, national development strategies and planning invariably involve plans for developing and/or strengthening participation in the fisheries sector. In addition, for economic security reasons the South Pacific states and territories place a high priority on the development of national industries (fleet and processing) as they consider that domestic industry affords them a greater degree of control over the sector. The high level of participation of foreign vessels in the tuna fisheries is seen as an intermediate solution, and the states and territories generally aspire to develop their fishery resources themselves. In the meantime, the Pacific islands have the objective of increasing the revenues from licensing fees in order to raise what they consider a more reasonable financial return from the exploitation of their resources. Most of the South Pacific states and territories also seek to diversify activities in the fisheries sector by encouraging the establishment of new industries, trying to integrate the fisheries sector more closely into the expanding tourist industry and, where possible, promoting inland fisheries and aquaculture.

Regional fisheries cooperation in the South Pacific is well-established, successful and, in many cases, a cornerstone of national foreign policy. States recognize that individually they are weak because they are small and can easily be manipulated in fisheries matters. It was primarily this recognition that led to the establishment, in 1989, of the Forum Fisheries Agency (FFA), which is mandated to assist its member countries to coordinate their fisheries policies and activities.5 The South Pacific Regional Environmental Programme (SPREP) assists member countries in respect of the adverse impact of human activities on fishes in coastal fisheries and, for reef and lagoon fishes, the South Pacific Commission (SPC) Coastal Fisheries Programme is developing a mechanism for greater harmonization of national policies. SPC also compiles fisheries data and provides scientific assessments in support of FFA’s conservation and management work. In addition, after the United Nations Conference on the Law of the Sea, the independent island states pooled their effective capacity for managing tuna fisheries probably to a greater extent than any other region. The Pacific island states, which generally lack any capacity for distant-water fishing, have taken a conservationist rather than an exploitative approach to the management of highly migratory species.

5 The members of the FFA are Australia, the Cook Islands, the Federated States of Micronesia, Fiji, Kiribati, the Marshall Is-lands, Nauru, New Zealand, Niue, Palau, Papua New Guinea, Samoa, the Solomon Islands, Tonga, Tuvalu and Vanuatu.In Australia and New Zealand, most fisheries are managed by licences and/or quotas and the import of vessels from abroad is monitored; hence the fleet is at, or around, the optimum size for harvesting the available resources. This is greatly aided by industry’s involvement in fisheries management. The reduction in the fleet has mainly been brought about by the buy-back of existing licences. In New Zealand, the introduction of individual transferable quota (ITQ) systems has greatly slowed down the pace of fishery expansion and led to greater fisheries rationalization. Finally, in both Australia and New Zealand, ITQs have enhanced economic efficiency within the fisheries sector.

The issue of by-catch discards is of most concern in trawl fisheries, but these are found only in Papua New Guinea’s Gulf of Papua shrimp fisheries, which has a by-catch of around 80 or 90 percent of the total, and very recently in the experimental scallop fishery in the Lagon Nord off New Caledonia (Box 6).

Many inshore and inland aquatic resources have declined as a result of overfishing and habitat degradation. Efforts to reverse this situation include the construction of artificial reefs, stocking, habitat improvement and the introduction of exotic species. Aquatic environments have been stressed and degraded by increased population growth (Box 7).

BOX 6

|

BOX 7

|

Fish and fishery products will continue to play a fundamental social and economic role in the South Pacific. Fish for human consumption will remain the most important source of animal protein for many Pacific island communities, in particular for the most disadvantaged ones. The fisheries sector will be one of the primary vehicles for promoting economic development in the South Pacific and, for some states and territories, the sector will be the main engine of economic development. Few areas or regions of the world will depend more on the fisheries sector for development than the South Pacific.

The region’s fisheries resources are probably capable of meeting a somewhat increased future demand for fish, although it is likely that additional amounts of pelagic species will have to be consumed, particularly in urban areas and in other areas of high population concentration. Marketing and distribution systems will need to be improved in order to move fish more quickly and efficiently both among states and territories in the region and within states and territories themselves. The promotion of sustainable fisheries and the implementation of regional and national arrangements to ensure that fisheries resources are utilized rationally are major social and economic policy issues in the South Pacific and most states and territories are attempting to deal with overfishing of inshore resources.

States and territories in the South Pacific recognize that effective and sustainable regulation of both inshore and offshore fisheries resources is essential for long-term food and socio-economic security.

The potential for aquaculture development varies significantly among subregions. Physical, biotechnical, economic, institutional and other issues generally disturb the development of aquaculture in the South Pacific, although the potential does exist for the selective and careful development of production for food and economic purposes.

With regard to trade, Australia and New Zealand are speciality product exporters to Japan, the United States and Europe. Exports have expanded in recent years, especially for New Zealand fishery products (e.g. mussels) and this is expected to continue. The forecast for New Zealand’s and - to a lesser extent - Australia’s seafood exports is positive, provided that sound management practices are enforced for deep-water species, such as orange roughy, which grow slowly.

In the SIDS, the forecast is for a contraction of fish imports and a small increase in exports, mainly tuna. Fresh sashimi-grade tuna is already transported by air to the Japanese market, but the distances involved and other problems will continue to hamper access to this lucrative market. Papua New Guinea might become an important exporter of canned tuna to the European market, once its cannery is fully operational - the advantages of the Papua New Guinea industry is that it is close to the resource and that the quality of the tuna is excellent.

1 This review is based on the regional study prepared by the FAO interdepartmental task force, headed by J. Cortez, Fishery Policy and Planning Division/International Institutions and Liaison Service (FIPL).

The region encompasses the marine and inland water jurisdictions of the following states: the Democratic People’s Republic of Korea Hong Kong, Japan, Macao, Mongolia, China, the Republic of Korea, the east coast area of the Russian Federation (the fisheries of the Russian Federation are summarized in the regional study on Europe on p. 64) and Taiwan (Province of China). The review will concentrate on the three most important fishing nations - Japan, China and the Republic of Korea - although the figures given for the region cover all countries, unless otherwise specified.

The seas within this region consist of the northwest Pacific Ocean including the Sea of Japan, the East China Sea and the Yellow Sea.

Fish production is an important economic activity in the East Asian coastal states. The region is one of the world’s largest fish-producing areas with a total production of 36.6 million tonnes in 1994.2 The East China Sea, the Yellow Sea, the Sea of Japan and the eastern offshore waters of Japan are among the most intensively fished waters in the world, and aquaculture production in the region contributed more than 70 percent of the total global volume. Fish consumption is generally high, exceeding meat consumption in some of the countries; annual food fish supply amounts to 21 kg per caput on average (live weight equivalent). The region is an active trading partner on the international market and a net importer (in both volume and value).

2 Including distant-water fishing by the fleets of the region and Poland’s distant-water fishing in this area.RESOURCES AND PRODUCTION

Marine fisheries

Marine fisheries landings by local fleets in the northwest Pacific reached a total of 22.6 million tonnes in 1994. Another 1.9 million tonnes were fished in other marine waters. The main fishing nations are China, followed by Japan and the Republic of Korea.

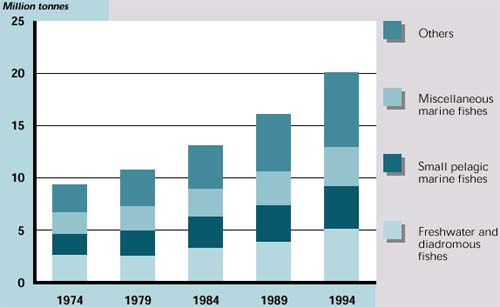

Figure 35. Regional fish production and share of world production in percentage

Fisheries in the East China Sea are usually small-scale, although larger trawlers are sometimes used. Tuna, mackerel, shrimp, milkfish, sea breams, croakers and shellfish of various kinds are the main species harvested. The demersal fish resources of the Yellow Sea have been exploited by trawlers from China, the Republic of Korea, the Democratic People’s Republic of Korea and Japan for years. The main resources are sea bream, croakers, lizard fish, prawns, cutlass fish, horse mackerel, squids and flounders. All species are overfished, and the catch of particularly valuable species has declined recently. The Sea of Japan has a range of pelagic and demersal species, including herring, pilchard, Alaska pollock, mackerels and bluefin tuna, but these resources have gradually been overexploited. Squid fishing is carried out in the central part of the sea, salmon fishing in the shoal areas and crustacean trapping in the deeper parts. The sea is heavily fished by fleets from Japan, the Russian Federation, the Republic of Korea and the Democratic People’s Republic of Korea.

Total marine production in the region has decreased over recent years, although 1994 landings represented a slight increase compared with the year before. The decrease is mainly associated with the decline of pelagic fish landings, in particular the Japanese pilchard; although it does not seem to be related to fishing but rather caused by decadal-scale changes in the marine environment (Box 8). However, other resources, particularly Alaska pollock, show low levels caused by heavy exploitation.

The two largest fleets in the region are the Japanese and the Republic of Korea’s, which, in 1994, had 2 423 and 1 012 vessels, respectively, of a gross registered tonnage (GRT) over 100 GRT/vessel. The Chinese fleet consisted of 253 vessels of over 100 GRT in the same year. In the Republic of Korea, the fishing industry faces difficulties from rising labour costs and the depletion of marine resources, and in some fisheries, such as the anchovy dragnet fishery and the Alaskan pollock fishery, high degrees of automation have been introduced. In addition, the government plans to adjust fishing capacity in national waters by reducing the overall tonnage by 137 000 GRT by the year 2004 although, over recent years, the total tonnage has increased somewhat despite the reduction in the number of vessels.3 In Japan, the number of vessels has also decreased during the 1990s, together with the number of fishermen and fishing enterprises. In China, fishing capacity in domestic waters has expanded far more than production. For example, the total power of Chinese fishing vessels operating in the East China Sea increased by a factor of about 7.6 times between the 1960s and the early 1990s, while catches only increased 2.6 times.

3 National Fisheries University of Pusan. 1996. Fisheries country profile. Pusan, Republic of Korea.

The heavy exploitation of most marine domestic fishery resources in Chinese waters and an emerging consumer market provided the impetus for China to develop a distant-water fishing fleet, first introduced in 1985. The Republic of Korea and Taiwan, Province of China, take most of their catches from local waters but have also extended their activities into distant water lately. In 1995, landings of the Republic of Korea’s distant-water fishing fleet were 0.9 million tonnes.

Japanese high sea catches decreased from 2.1 million tonnes in 1970 to 0.9 million tonnes in 1993 and are expected to decline further as Japanese fishing companies find it difficult to compete with imported fish and fish products.

BOX 8

|

Inland water fisheries

Production from freshwater capture fisheries in the region continues to be dominated by China, which generated over 1 million tonnes out of a regional total of 1.4 million tonnes in 1994. However, environmental degradation combined with overfishing have affected capture fisheries in all major Chinese rivers, particularly in stretches downstream of significant pollution sources. This has resulted in significantly reduced yields and the loss of many commercially valuable species. In contrast to the declining contribution of river fisheries, increased yields are being achieved through intensified exploitation of natural lakes and reservoirs, mainly from enhancement measures such as improved stocking, fertilization, the control of unwanted species, habitat modification and environmental engineering of the water bodies.

Aquaculture

Total regional aquaculture production amounted to 18.4 million tonnes and valued US$22.8 billion in 1994, representing 73 and 57 percent of the total world production, respectively. During the period 1984 to 1994, the subsector demonstrated a compounded yearly growth rate of 10 percent in volume and 11 percent in value.

China is by far the most important producer, representing over 60 percent of world aquaculture production - 15.4 million tonnes in 1994. Finfish production is concentrated in China, where it is cultivated at low stocking densities within semi-intensive, polyculture, pond-based farming systems. The main species cultured are cyprinids such as silver carp, grass carp, common carp, bighead carp and, more recently, tilapia.

Chinese production patterns contrast sharply with finfish production in Japan, which is restricted almost entirely to high-value carnivorous marine and diadromous species grown in intensive farming systems. The two major species are yellowtail and red sea bream. Aquatic plants constitute the second most important species group by weight and value. Molluscs and crustaceans are also produced.

Sea ranching is also practised in Japan, where about 80 species are targeted by sea farming (including some that are under technical development). The main species ranched are silver sea bream, bastard halibut, kuruma prawn, swimming crab, abalone and sea urchin.

Growing environmental concern is an increasingly important isssue for future aquaculture development in the region (Box 9).

Figure 36. Fish utilization and food supply

Figure 37. Fishery imports and exports (including intraregional trade)

N.B. FAO trade statistics available only from 1976PRODUCTS AND MARKETS

Fish consumption in the region is very high by international standards; average annual food fish supply is 21 kg per person (live weight eqivalent) and fish provides about one-quarter of the total animal protein intake. Particularly in Japan, the tradition of eating fish is very strong and fish is generally more important than meat in the diet, even though younger generations today tend to eat more meat than before. The per caput food fish supply in Japan is over 70 kg per year. Although fresh fish is preferred, demand is diversified and includes an increasing share of both traditional and new processed products. At present, about two-thirds of the fishery production is used as raw material for the processing industry but both the fishing and the processing industries are being rationalized and operations are increasingly relocated to foreign countries through joint ventures and other arrangements because of lower labour costs and preferential access to raw material.

During the last decade, imports have expanded considerably and international trade in the region focuses on Japan, the world’s major importer of fish and fishery products. About one-third of the world fish trade goes to Japan (in value terms) and Japanese imports of fishery products increased fourfold over the decade to 1994. The main imports were shrimp and prawn, fresh and frozen tuna, crab and salmon (in value) and shrimp, prawn and tuna (in quantity).

Statistics for the Republic of Korea and Hong Kong show per caput food fish supplies of about 50 to 55 kg per year. In the Republic of Korea, captured fish is generally preferred to cultured fish and fresh fish is generally preferred to processed products. Nevertheless, the number of processing plants in the country seems to be increasing.4 The Republic of Korea is both a major importer and an exporter. In the past, high duties have protected the fishing industry from imports of cephalopods and other fishery products and, as a result, the price of squid was among the highest in the world. However, as of 1995, the Republic of Korea has liberalized over 300 product items and will open its markets fully for fish products by 1997.

4 National Fisheries University of Pusan, op. cit., footnote 3, p. 58.

BOX 9

|

In China, the mean per caput supply was reported as 10 kg in 1990, but consumption has probably increased significantly since then. However, important variations exist within the country; in the southern parts, particularly in Guangdong province, the average is 43 kg, whereas fish consumption in the isolated areas of the northeast is negligible. Domestic demand is largely met by freshwater pond products, in particular various carp species; in 1993, over half of Chinese fish production originated from culture fisheries. The current increases in disposable income in China are creating market opportunities for fish imports. One of the main fish imports at present is Alaska pollock from the Russian Federation, which is processed and re-exported to the United States and Germany. Shrimp is also imported for processing and re-export to the United States.

FISHERIES POLICY AND MANAGEMENT

The restricted circulation of ocean waters into and out of the East Asian seas apparently makes them particularly sensitive to environmental changes from human or natural causes. In the Republic of Korea, industrial complexes near coastal areas and an increase in the influx of sewage from the urban zones are harming coastal fishing grounds. Moreover, land reclamation projects are reducing the fishing ground areas and oil pollution as well as red tides have occurred, particularly in the south.5 Similar developments are taking place also in other parts of the region.

5 Ibid.

Providing more than a third of the world’s fish landings also means that the region produces a similar amount of by-catch. However, the proportion of the by-catch that is discarded is likely to be lower than this, particularly in China; although there is very little detailed information available on this issue.

Figure 38. Fishery production by species categories

Figure 39. Fishery imports and exports for major trading countries in 1994

International fisheries issues in the region have been dealt with through bilateral fisheries agreements, such as those between Japan and the Republic of Korea and between Japan China. The Russian Federation has established an exclusive economic zone (EEZ); so has Japan for its east coast, but this EEZ is not applied to China and the Republic of Korea. In the region, efforts to avoid unnecessary controversies over potential maritime jurisdictional overlaps are evident. Regional cooperation (except for Taiwan, Province of China) is also carried out through the newly reconstituted Asia-Pacific Fishery Commission (APFIC), a regional fisheries body established under FAO. Likewise, coastal states (except the Democratic People’s Republic of Korea) have become members of the Fisheries Working Group of Asia Pacific Economic Cooperation (APEC).

In the Republic of Korea, the Fisheries Act was amended in 1995 to accommodate new international management schemes and reflect the relevant provisions of the UN Convention on the Law of the Sea and other international rules and provisions related to fisheries. In response to the increasing regulation of the high seas and the deterioration of resources in the waters around the Republic of Korea, the government initiated a fisheries restructuring project in 1994 to reduce the number of fishing vessels. In addition, to tackle environmental degradation, the government has designated a number of “fisheries resource conservation areas” and increased research efforts on pollution-related matters.6

6 Ibid.

Japan has a unique and comprehensive system of fisheries management. Coastal and inland fisheries are regulated by fisheries cooperatives through a system of fishing rights; offshore and long-distance fisheries are managed through licensing. The Fisheries Law and the Fisheries Resource Protection Law form the legal basis for fisheries management with broad authority given to the Ministry of Agriculture, Forestry and Fisheries, as well as to the prefectural governors. In the future, improved fishery management is expected to focus on increasing the production of high-value species, using traditional management techniques (regulation of effort or catch, closed seasons and areas), community-based management and innovative approaches to remedying damaged environments to favour habitat, growth and the recruitment of preferred high-value species. Co-management and regional cooperation will also be stressed, and the introduction of EEZs could be expected. Japan will also probably have a more integrated view of the whole fishing and processing industry as links among markets, trade and resources become stronger and more apparent.

China has adopted a pragmatic approach towards developing its fisheries institutions and administration, and is developing managerial capabilities. This is being further strengthened by appropriate legal provisions such as the Fisheries Laws and Regulations for the Conservation and Propagation of Fishery Resources. China appears to face the same fishery and coastal zone management issues as other countries in the region, including the need to create alternative employment opportunities for inshore fishers, intersectoral competition, environmental pollution and habitat destruction. In addition, as provincial governments become more autonomous, interprovincial coordination will be urgently required to resolve conflicts over shared resources and environmental degradation.

OUTLOOK

Fish consumption in the region should stay high and even increase further in some areas (in both volume and per caput levels) along with population growth and improved consumer purchasing power.

An exception to this may be Japan, where fish consumption is already high and population growth close to zero. Nevertheless, the composition of the Japanese fish consumption basket is expected to continue to change from lower-value to higher-value products, which could include more “ready-to-eat” products as well as products sold through fast food outlets. The sophisticated nature of fish consumption attitudes has important bearings on domestic production strategies which need to focus on those types of products where Japanese producers have a clear competitive advantage over foreign suppliers, for example, ranched products which can be marketed as “fish from the wild” rather than cultured products. Sea ranching is expected to become the preferred form of culturing finfish species. Future fisheries development in Japan will be guided largely by market factors, especially the ability of the domestic industry to compete with foreign suppliers. Japanese fisheries are unlikely to grow significantly over the coming decades. Modest production gains from culture and ranching are likely to be offset by a further decline in the long-distance fleets, but the country will continue to rely on imports to satisfy its high demand for fishery products.

Similar consumption patterns can be seen to some extent in the Republic of Korea, which is currently liberalizing its trade regulations on fishery products and is one of the places where imports could be expected to increase in the future. However, at the same time, the Republic of Korea remains an important exporter. For domestic production, priority is given to enhancing the utilization of national fishing grounds through the construction of artificial reefs and fingerling releases. Aquaculture is also becoming a more important source of fishery products.7

7 Ibid.

In China, the expected continuation of both rapid economic growth and expanding fish production will enable per caput consumption to increase further. Significant growth potential exists for freshwater aquaculture, principally through the rehabilitation of existing ponds, the utilization of water-logged areas and the vast surface areas of paddy fields. The growing number of hatcheries will enable this potential to be realized. Traditional marine capture fisheries do not appear to offer any significant growth potential. Coastal fish resources need to be carefully managed and future increases in landings will probably depend on distant-water fishing. However, strong economic growth is expected to generate enough purchasing power to satisfy any domestic demand-supply gap with imports.

1 This review is based on the regional study prepared by the FAO interdepartmental task force, headed by R. Grainger, Fishery Information, Data and Statistics Unit (FIDI).

The region covers two main groups of countries: 1. The European industrialized countries comprising the European Union (EU) and the European Free Trade Association (EFTA), i.e. the European Economic Area (EEA), as well as Malta, Andorra and Monaco; and 2. the former centrally planned economies - or transition countries - of Eastern and Central Europe including the Russian Federation and the other European republics of the former USSR. The main seas neighbouring the countries of the region are the northeast Atlantic (including the North Sea, the Baltic Sea, the Norwegian Sea and the Barents Sea), the Black Sea, the Mediterranean Sea and the northwest Pacific (the Bering Sea and the Okhotsk Sea).

Fish production is important to many countries of the European region, in particular as a foreign exchange generator in the transition states and as a source of employment in coastal communities. Regional fleets produce 16 percent of world fishery production volume, i.e. 17.2 million tonnes. Per caput fish consumption varies from high average levels in some of the Mediterranean and Nordic countries, where there are food fish supplies of over 30 kg per year (live weight equivalent), to 10 to 15 kg per year in some of the transition and inland countries. The region is a net importer, by both value and volume.

RESOURCES AND PRODUCTION

Marine fisheries

Total regional marine catches amounted to 15.3 million tonnes in 1994.2 The fleets of the industrialized countries caught about 70 percent of this total. The production of the western subregion is dominated by catches from the northeast Atlantic, where herring, sand eels, capelin, cod, mackerel, pilchard, sprat, horse mackerel, blue whiting and saithe are among the main commercial species. Further north, in the northeast Arctic and Barents seas as well as in Icelandic and Faeroe Island fishing waters, cod and capelin are the most common species fished, together with herring, haddock and saithe. In the Baltic Sea, cod, herring, sprat and salmon are fished.

2 Including distant-water fishing production.

Figure 40. Regional fish production and share of world production in percentage

Nevertheless, many demersal groundfish stocks have been intensively exploited during the last decades and some of the stocks are now considered to be outside the safe biological limits. Small pelagic resources are generally less affected. In addition, pollution has caused environmental deterioration in some coastal areas of the north Atlantic. With regard to salmon in the Baltic Sea, wild stocks are threatened by disease and competition from reared stocks (Box 10). In the Mediterranean, most demersal stocks are also fully to overexploited. Consequently, in addition to fishing in nearby waters, the European Union (EU) fleets increasingly seek access to other countries’ exclusive economic zones (EEZs) for their distant-water vessels and budget funds for access agreements have been increased recently.3 Iceland and Norway also carry out fishing under a number of bilateral agreements.

3 Fishing News International. 1996. Review of Europe’s fishing deal.

The main fishing areas of the eastern subregion are the Okhotsk and Bering seas in the northern Pacific Ocean. The most important species in the northern Pacific is the Alaska pollock, although landings in 1994 of 2 million tonnes were only half of those in 1986. Fishing by the fleets of the transition countries is also carried out in the Barents Sea, mainly by Russian vessels fishing cod, and in the Baltic Sea by Estonia, Lithuania, Latvia and the Russian Federation.

Total catches in the Black Sea dropped drastically from 913 000 tonnes in 1988 to 277 000 tonnes in 1992,4 but recovered to 511 000 tonnes in 1994. The reason for the decline seems to be a change in the ecosystem caused by a combination of uncontrolled and heavy fishing, nutrient input from rivers and littoral zones, as well as the introduction of exotic species.

4 The total catch of the Black Sea includes catches by countries outside the region.

Fleet technology in the industrialized countries is very high and there has been a shift from labour-intensive to more capital-intensive vessels. Nevertheless, investment in demersal fishing vessels has generally decreased recently. Instead, investments have been directed towards pelagic fisheries and the processing industry. There is a critical overcapacity in the European fisheries; a recent EU review indicates that a reduction of 40 percent in overall fleet capacity is needed in order to downscale the size to match the available fish resources.5

5 Report of the Group of Independent Experts to Advise the European Commission on the Fourth Generation of the Multi-annual Guidance Programmes. 1996.

The marine production of the former centrally planned economies and the former USSR (the eastern subregion of Europe) decreased from about 10 million tonnes yearly at the beginning of the 1980s, to only 4.5 million tonnes in 1994. The main fishing nation, the Russian Federation, represented 3.5 million tonnes of the total in 1994. An important reason for this drastic decline is the reduction in distant-water fishing activities; the former USSR, Poland, Romania and Bulgaria used to have large distant-water fleets and, in 1983, about 40 percent of the production of these countries originated from distant-water fishing but, in 1993, this share had decreased to 20 percent. The fleets of the transition countries are generally old and in great need of modernization. The Russian Federation started an ambitious programme of fleet renovation in 1994 and there have been some signs of recovery, with the Russian Federation and Poland increasing their catches by about 20 percent in 1995.

BOX 10

|

Inland water fisheries

Capture fishery production from the region’s inland waters has decreased by almost 50 percent during the last decade, falling from 820 000 tonnes in 1984 to 420 000 tonnes in 1994. The main species include rainbow trout, Azov Sea sprat and common carp. It should be remembered, however, that official data for inland water capture fisheries may in many cases be underestimated. Production from subsistence and recreational fisheries is seldom accurately reflected in the statistics and it is likely that production from these sectors plays a rather important role for food supplies in the transition countries. Nevertheless, commercial catches have declined owing to political changes and the collapse of infrastructure and distribution systems in the former centrally planned economies. Pollution, infrastructure projects and competition for water resources from other sectors have also had a negative impact on fisheries production. All countries in the eastern subregion used to manage their inland fisheries through stocking and fertilization programmes to enhance capture fisheries. In the Russian Federation, this activity is still being subsidized, whereas it appears that the practice has been discontinued in other countries owing to the economic difficulties inherent in the transitional period.

In the industrialized countries, inland waters are managed primarily for sport fisheries; commercial fishing is secondary except in the large lakes. The stocking of selected species, such as rainbow trout, stringent antipollution laws and rehabilitation programmes are common components of the management programme for these fisheries.

Aquaculture

In 1994, regional aquaculture production accounted for 6 and 10 percent of total global production in quantity and value, respectively. In 1994, 1.5 million tonnes were produced at a value of US$3.8 billion, of which 1.3 million tonnes came from the industrialized countries and 195 000 tonnes from the transition states. In the former, about half of production is molluscs6 and the second largest component is diadromous fish, i.e. salmon and rainbow trout. In fact, the aquaculture sector has undergone a revolution because of the success of, in particular, salmon farming.

6 It should be noted that for molluscs only about 10 percent of the gross weight is actually consumed; the greater part of the production volume is shell.

In the eastern part of the region, total production fell by half between 1991 and 1992 owing to economic and social difficulties when the centrally planned system collapsed. This decline was felt most in the countries of the former USSR; production in Hungary, Poland and former Czechoslovakia remained more stable. Farming of carp (Chinese and common carp) and other cyprinids is most common even though the production of higher-value species is being introduced and a further switch could be expected when production levels revive.

Figure 41. Fish utilization and food supply

PRODUCTS AND MARKETS

Almost all European industrialized countries have some kind of processing industry such as canning, smoking, freezing or otherwise curing of fish. There is also a fishmeal industry in the region. The production of convenience food is the fastest growing sector of the EU fish processing industry and large retailers in the market are active in introducing new products. There is also a trend in some countries towards more fresh and chilled fish and supermarkets are increasing their market share of fish sales.

In the transition countries, much of the processing industry needs modernization and new investments. During the Soviet era, some of the coastal countries and republics had an important processing industry (e.g. Estonia, Latvia and Lithuania) of which only a portion is used today, following the fall in raw material supply. Moreover, in the past, the distribution of fish and fishery products was carried out by large state-owned companies which failed to survive the transition. The old system has not yet been fully replaced, but new private distribution companies and supermarket chains are emerging - through joint ventures - together with a wholesale infrastructure. Likewise, some of the processing plants have been modernized and are now producing value-added products that meet EU standards for export. Only Poland still has substantial processing facilities at sea; fish is frozen on-board distant-water fishing vessels and exported, mainly to the EU.

Figure 42. Fishery imports and exports (including intraregional trade)

Fish consumption levels vary considerably among subregions and countries. In the region as a whole, average per caput food fish supply was 17 kg (live weight equivalent) in 1994. However, in the industrialized countries the average supply is about 22.5 kg per year, with variations between, for example Iceland, where the mean fish supply per person and year is over 90 kg, and Albania, Bosnia, Croatia and the Federal Republic of Yugoslavia, where supply is less than 2 kg. In general, however, consumers’ perceptions of fish are positive and the demand for fish is likely to increase in the future. This volume cannot be supplied by local production and the area is a net importer of fishery products. In the EU, fish is the second largest food import item, although members of EU 12 accounted for 20 percent of world fish exports in 1994; this includes the value of intraregional trade.

Figure 43. Fishery production by species categories

A recent development in the region is the exertion of consumer pressure on the fishing industry to foster environmental objectives. Initiatives within this area include improved marine stewardship under the Unilever/World Wide Fund for Nature’s ecolabelling of products, the agreement by Unilever and Sainsbury not to use fish oil from industrial fisheries, the proposed import ban on cultured shrimp in Sweden and packaging laws in Germany.

In the transition countries, fish consumption has fallen dramatically recently owing to the lack of supplies; in the Russian Federation, annual per caput consumption decreased from 29 kg to 9 kg between 1989 and 1993. With regard to trade, traditional import and export patterns have changed completely over recent years. Eastern Europe and the republics of the former USSR are now increasingly exporting high-value species in order to generate foreign exchange - groundfish species such as Alaska pollock and cod are among the most common of these. At the same time, low-value products are being imported increasingly as local production decreases. The region is a net fish importer in volume but the value of exports exceeded that of imports by US$1.2 million in 1994.

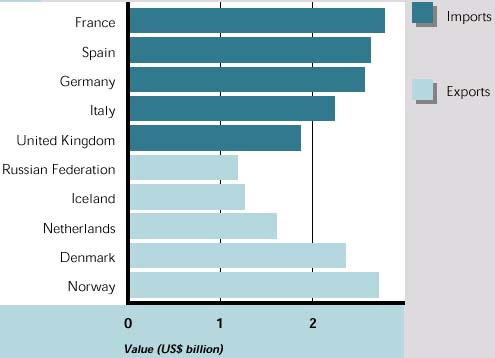

Figure 44. Fishery imports and exports for major trading countries in 1994

FISHERIES POLICY AND MANAGEMENT

In the new republics of the former USSR, the fisheries administrations are newly established government entities because in the past the sector was centrally managed from Moscow. During the years of transition, the administrative structure has undergone several changes and may still need modifications, such as a strengthening of the socioeconomic capacity. In spite of the availability of excellent natural scientists, qualified social scientists are usually lacking and the concept of planning the sector needs to be (re)introduced. So far, fisheries policies have concentrated on maintaining access to distant-water fishing grounds, improving fisheries management in the national zones and, as appropriate, harmonizing national legislation with that of the EU. Efforts have been made to restructure and privatize the fisheries sector in all countries, but obstacles such as high interest rates have often been encountered.

BOX 11

|

In the EU, there is a Common Fisheries Policy (CFP), parallel to the Common Agriculture Policy, “with common rules throughout EC member countries covering all aspects of the fishing industry from the sea to the consumer”7 (Box 11).

7 European Commission. 1994. The new Common Fisheries Policy. Luxembourg, European Commission, Directorate-General XIV Fisheries.

A number of fisheries management systems exist in the region. The EU Common Fisheries Policy uses a system of total allowable catch (TAC) and quota allocations supplemented by technical measures. In the Baltic Sea, TACs and national quota allocations are agreed by the International Baltic Sea Fishery Commission (IBSFC) based on advice from ICES, which also gives management advice for other parts of the northeast Atlantic. In the Mediterranean, individual countries set national policies which differ by country although the EU coordinates the national policies of its members with advisory inputs from the General Fisheries Council for the Mediterranean (GFCM). Management focuses on measures such as controls of licences and subsidies to the sector, rather than quota control. There is also a serious lack of information on the actual status of stocks. In the Black Sea, no quota or effort controls apply and there is a considerable degree of fleet overcapitalization. A new convention for a Black Sea Commission is now being negotiated among the coastal states.

BOX 12

|

Discarding is a serious issue in the region. The northwest Pacific has the highest discard volume in the world, estimated at 9.1 million tonnes, followed by the northeast Atlantic with 3.7 million tonnes. In the Atlantic, the phenomenon appears in part to be a consequence of single species management by quota in what are mixed species fisheries, encouraging “high grading” and discard practices that can sometimes approach 50 percent of the demersal catches although the general absence of observers on-board commercial vessels makes quantification difficult. Norway, as one of the major fishing nations in the area, has introduced a no-discards policy (Box 12). In the Mediterranean and Black seas, discard problems may be less acute, except for the large-scale gill-net fisheries which still operate despite the UN ban.

Other problems facing fisheries management organizations and arrangements in the northeast Atlantic include pollution, misreporting and a lack of appropriate enforcement. The North Sea Task Force8 has undertaken one of the most comprehensive quality status reports ever made for a marine ecosystem and made recommendations for the development of a strategy to protect species and habitats.9

8 Members of the task force are the eight North Sea states - Belgium, Denmark, France, the Netherlands, Germany, Norway, Sweden and the United Kingdom - as well as relevant representatives of the European Commission.9 North Sea Task Force. 1993. North Sea Quality Status Report 1993.

A major problem is referred to as “black fish landings”, i.e. unrecorded landings that are made to avoid quota restrictions. Efforts to improve monitoring, control and surveillance (MCS) capabilities have included the use of vessel monitoring systems, and the EU intends to implement further post-harvest audits of logbooks and sales documents.

Traditional management methods of catch limitations have repeatedly failed to reduce fish mortality in the northeast Atlantic and are largely discredited. A major reduction of fleet capacity as well as more extensive use of direct fishing effort control, as is currently being considered by the EU, could prove more effective.

OUTLOOK

The demand for fish in Europe is likely to increase in the future, given the positive perception of fish as a food item in the western part of the region and the recovery of previous consumption levels in the eastern part. However, for rapid recovery, supplies of inexpensive products will be needed.

Fish production in the transition countries, in particular the Russian Federation, should stop declining soon and start to recover slowly. The revitalized fishing industry will be very different from that of the 1980s; it is likely that the distant-water fishing sector will play only a minor role and that emphasis will instead be on better utilization of resources in home waters. A sound restructuring programme would include a renovation of the fleets - as already started in the Russian Federation - and a reduction of overcapacity in the fishing sector.

Future fishing prospects for the industrialized countries depend mainly on the effectiveness of fisheries management in the northeast Atlantic. As mentioned above, the elimination of overcapacity and a more direct control of fishing efforts could be two components of a scheme for improved management.

Inland fishery resources are already considerably exploited, and their main orientation is changing from food production to recreation. Nevertheless, some increases in food fish production from inland waters - especially in the transition countries - could be achieved by better management. Although aquaculture production may increase in western Europe, it is likely to be constrained by limited site availability, competition for aquatic resources, stricter environmental controls and cheaper imports from other regions. However, given the potential markets in industrialized countries, aquaculture production in transition countries is likely to diversify into the culture of higher-value species such as salmon and eels.

Trade in fishery products has continued to grow, albeit at a slower rate, over the last three years. In order to meet future demand, the region as a whole will continue to be a net importer of fish.

1 This review is based on the regional study prepared by the FAO interdepartmental task force, headed by A. Gumy, Fishery Policy and Planning Division/Development Planning Service (FIPP).

The region covers the South American continent, Central America and Mexico, as well as the island states and territories of the Caribbean. The region is surrounded by the southern parts of the Atlantic and Pacific oceans and includes the semi-closed seas of the Gulf of Mexico and the Caribbean Sea.

Latin American and Caribbean fish production reached record levels in 1994 of 24 million tonnes, representing 22 percent of the world total. Small pelagic marine fish make up about 75 percent of the total catch. The contribution of the sector to the economy is highly concentrated in coastal rural areas where it is the key - and often only - source of employment and income. Internally, it plays a minor role. Food fish consumption has been less than the global average at a per caput supply of about 9 kg annually (live weight equivalent). Latin American countries are major exporting countries of fish and fishery products and account for 11 percent of world exports, with Chile as the main net exporter. Shrimp and fishmeal are the main exports.

RESOURCES AND PRODUCTION

Marine fisheries

Total marine landings in the region amounted to 23.1 million tonnes in 1994, 85 percent of which derived from the southeast Pacific, where catches reached a record high in that year. Total production is still dominated by Peruvian anchoveta and fluctuations in total volume are the result of this species’ variability. Catches from anchoveta fisheries collapsed in the 1970s from 13.1 million tonnes in 1970 to 1.7 million tonnes in 1973 and down to only 94 000 tonnes in 1984. Since then the stock has recovered and landings reached 11.9 million tonnes in 1994. While heavy fishing played a major role in the collapse, climatic change through the El Niño was also a primary cause of recruitment failure and stock decline (Box 13). Although the two main substocks of the Peruvian anchoveta are now reported to be fully exploited, rigorous monitoring and surveillance measures are necessary to avoid overfishing.

Other small pelagic stocks such as the South American pilchard, the Chilean horse mackerel and mackerel started to increase when the Peruvian anchoveta fishery collapsed; the first two species are now major components of production in the area, although the pilchard is considered fully exploited and even overexploited in part of its range.

In the southwest Atlantic, production has been increasing recently. The dominant species are squid and hake, followed by basses, congers and other demersals. Squids, shrimps, lobsters and crabs, as well as small pelagic species such as sardinella and Argentine anchoveta, are also fished. Until the 1980s, this was one of the few fishing areas of the world to have a large expansion potential but, since then, several industrialized long-range fisheries have developed and most of the fish stocks are now considered to be fully exploited, while some have been overexploited over the last few years.

Figure 45. Regional fish production and share of world production in percentage

In the western central Atlantic area, most pelagic fisheries, including billfish, tuna and swordfish, are fully or overexploited. There is general concern about finfish, especially sharks and rays, and many species of reef fish have been fully or overexploited, as has the queen conch. In the eastern central Pacific, fish production has generally decreased despite a slight increase between 1993 and 1994. The most dramatic steady decline in catch since the mid-1980s has been in the Californian anchovy and sardine fisheries, which has had a negative impact on Mexican production levels. The production of tunas and other large pelagics has also increased slightly over the past 20 years. Shrimps and prawns sustain particularly valuable and important fisheries throughout the area.

While the Latin America region depended heavily on imported vessels and fishing gear in the past, recently more up-to-date, harvesting technology has been transferred to the region, in particular from northern Europe. Regional shipyards can now build and fit fishing vessels to high standards while local manufacturers can make every type of fishing gear and gear handling machinery. This transfer is reflected in the large and state-of-the-art equipped purse seiners built by yards in both Peru and Chile. In the southern part of the Pacific, purse seining for small pelagics is a very large-scale operation aimed mainly at supplying raw material to fishmeal and fish oil plants. In the north, shrimp trawling is more common. On the Atlantic coast, the main harvesting methods vary from trawling for shrimp and demersal species with medium-sized vessels in the region north of the Amazon river, to larger-scale bottom and midwater trawling by large freezer stern trawlers south of the River Plate. In addition, there is a seasonal purse-seine fishery for small pelagics in southern Brazil and important tuna purse-seine fisheries in Venezuela. Longlining is also practised all along the coastline.

BOX 13

|

In the small island Caribbean states, fisheries are mainly small-scale and artisanal, utilizing passive gear such as hooks and lines, gill-nets and pots and traps. In most cases, artisanal vessels are traditionally built for harvesting demersal resources and crustaceans close to the islands.

According to data from Lloyd’s Maritime Information Services, the Latin American fleet has been increasing at an annual rate of about 5 percent over the last decade. Even allowing for the open ship registers of Panama and Honduras, there has been an increase in the number of large vessels in the region. Lloyd’s Register of Shipping shows a total of 3 156 vessels with a tonnage exceeding 100 gross registered tonnage (GRT) registered in the region in 1995, compared with 2 238 in 1985.2 This expansion of the industrial fishing fleet has meant excess fishing capacity is now an issue, even in several hake and tropical shrimp fisheries.

2 When the fleets of Honduras and Panama are excluded, the corresponding figures are 2 152 in 1995 and 1 787 in 1985.

Inland water fisheries

After rapid growth in inland fisheries production up until 1987, when the combined regional catch topped 580 000 tonnes, catches stabilized and even declined to about 450 000 tonnes in 1991. In 1994, total reported catches attained some 500 000 tonnes, which is far below the potential yield for the inland waters of the continent and much lower than reported production from similar areas of the tropics in Africa and Asia. These falling figures may partly be owing to inadequate statistics (generally data for recreational and subsistence activities are not recorded), but are probably mainly attributable to generally low productivity.

Inland fisheries are concentrated in areas near the main water courses. Although exploitation is low, localized regions show signs of overfishing. Elsewhere the effects of overfishing have been exacerbated by environmental degradation. Three main exploitation patterns characterize the region: in the south, i.e. in Argentina, Chile and parts of Brazil, commercial fisheries have usually been closed and resources are now reserved mainly for recreational and subsistence activities; in the central part of the region, commercial fisheries on rivers and reservoirs are less intensive; and in the north, particularly in the drought polygon of Brazil, in Cuba and in Mexico, an increasing trend towards the intensive management of reservoirs through stocking and species introductions has led these areas to record the highest growth in recent years.

Most Caribbean islands do not have any inland waters of importance; consequently inland water fisheries are virtually non-existent there.

Aquaculture

In 1994, total aquaculture production reached 472 000 tonnes, representing about 2 and 5 percent of world production by volume and value, respectively. Aquaculture makes a similar contribution to total regional fisheries production, with six countries accounting for most of the production. Shrimp culture has increased very rapidly and represented over 80 percent of the total value of regional production in 1994. Salmon culture has also developed, although almost exclusively in Chile. However, profit margins for both species have been declining. Freshwater fish and mollusc cultures are also carried out, for example tilapia, trout and carps.

Figure 46. Fish Utilization and food supply

Industrial export-oriented aquaculture has expanded significantly and still has moderate growth potential. Finally, aquaculture oriented towards producing low-cost products has developed to a minor extent.

PRODUCTS AND MARKETS

Fish consumption levels vary widely among countries as well as within countries. The regional average of per caput food fish supply is around 9 kg annually (live weight equivalent), which is well below the world average of about 13 kg. However, consumption has been increasing slightly over the last decades. For about 5 percent of the total population, i.e. for the inhabitants of the English-speaking Caribbean islands and of Chile, per caput annual supplies top 30 kg. Conversely, most Central American countries show levels of less than 5 kg per year. As a result, the contribution of fishery products to animal protein supplies is less critical in Latin America than in many other developing countries, although fish is still a vital food item in some local communities.

Figure 47. Fishery imports and exports (including intraregional trade)

The abundance of small pelagic fish provides the basis for an important fish reduction industry in Latin America, where more than two-thirds of the total catch are oriented to non-food products. The main items are fishmeal and fish oil used as feed in the animal husbandry, poultry and aquaculture industries. Chile, Peru and, to a lesser extent, Ecuador use the bulk of the raw material destined for fishmeal. Other non-food uses, such as for bait and pet food, do not represent substantial shares of fisheries output. Long-standing efforts have been made to reduce the quantities used for fishmeal production and to find alternative uses for direct human consumption but no sustained success and economic feasibility have been achieved to date, largely owing to the ready availability of fishmeal raw material and reluctance to invest in market development.

Figure 48. Fishery production by species categories

The disposition of catches for direct human consumption shows the important share of fresh fish, i.e. over 50 percent, with frozen and canned in the order of 20 percent each. The utilization of fish supplies by processing type has generally followed historical patterns determined by the available resources and market forces, in particular international demand. Although the international market still prevails, the industry now seems to be more eager to adapt available technologies to any positive domestic market trends. Naturally, fish utilization varies at the subregional level - in the Caribbean, for example, fish utilization is influenced by the requirements of tourism.

Figure 49. Fishery imports and exports for major trading commodities in 1993

Latin American countries are major exporters of fish and fishery products, accounting for 11 percent of world exports. Equipped with modern processing plants, the region can manufacture to international standards and ensure safe and wholesome products. Shrimp and fishmeal are the main exports. Chile and Peru dominate the world fishmeal market, with exports going mainly to the Asian market, and Mexico and Ecuador are exporters of shrimp. Most Latin American shrimp exports go to the United States market; only recently have Ecuadorian shrimp exporters managed to penetrate the European shrimp market. While the Mexican shrimp export industry is still dominated by wild shrimp, Ecuador almost exclusively exports cultured shrimp products. Tuna has traditionally also been one of the main fish exports but the enforcement of a “dolphin-safe” policy by the United States Government in 1991 created substantial problems for Latin American tuna fisheries.

As fish-importing countries, Latin America makes up only about 2 percent of the world total. Intraregional trade is also still quite limited.

FISHERIES POLICY AND MANAGEMENT

In most countries, fisheries policy has been strongly influenced by macroeconomic policies that form part of stabilization programmes. Measures include the privatization of production units, the facilitation of foreign trade, reduction or elimination of economic incentives and providing incentives to foreign investment in the fisheries sector. These policies have also aimed at streamlining the administrative and technical structures of public administrations, including fisheries administration. In the transition period, the research and management capacity of fisheries administration has been affected in terms of functions, budget allocation and technical and administrative staff. Lately, however, the situation seems to have improved in several countries.

Most regional fishing nations have legal provisions to regulate and limit access to their main fisheries through various types of licensing schemes that regulate or limit the total number of vessels, fishermen, gears, accumulated engine power or other unit of fishing capacity that can enter most major fisheries. As a result, fisheries recognized to be near, or at, the state of full exploitation are theoretically under a closed-access regime, meaning that no new fisher can enter without replacing an existing one. Some countries also use individual quota systems to allocate access to resources, thus keeping fishing capacity under control. Individual transferable quota (ITQ) regimes are not in force at present in any nation of the region but a few countries are contemplating setting them up in some fisheries after assessing the technical and socio-economic factors involved.

National legislation to keep fishing capacity under control has not always proved very successful in the region. While the actual legislation may be adequate, non-existent or over-permissive surveillance and enforcement practices might be a major cause of excess fishing capacity in some highly profitable fisheries.

The regional institutional framework for fisheries cooperation, management and development is formed by several regional bodies. These bodies differ totally or partially from one another in legal nature, membership, areas of competence, mandate and geographical coverage. Two of them are FAO bodies: the Western Central Atlantic Fishery Commission (WECAFC) and the Commission for Inland Fisheries of Latin America (COPESCAL); the rest are non-FAO intergovernmental organizations such as the Organization of Eastern Caribbean States (OECS), the Caribbean Community and Common Market (CARICOM), the Permanent South Pacific Commission (CPPS) and the Latin American Organization for Fisheries Development (OLDEPESCA).

Latin American fisheries generally account for a rather small percentage of total discard volumes, estimated at around 5 percent. This relatively low figure is mainly owing to the high landings by Peru and Chile of fishmeal species, which yield very few or no discards. These two countries were reported to land 18.6 million tonnes of sardines, anchoveta and jacks mainly for their fishmeal industries, leaving the remaining catch of the area as less than 4.8 million tonnes. Nevertheless, these fisheries still generate some waste (Box 14).

Coastal area degradation is reducing the fishing potential in many places, particularly in small-scale fisheries. These fisheries continue to play a key role in supplying food and employment in marginal coastal areas and several countries are taking steps to introduce integrated coastal area management approaches as an alternative to other resource management schemes.

OUTLOOK

Fish consumption in Latin America and the Caribbean has been increasing gradually over the last 20 years and will probably continue to increase in the future. Taking population and economic growth into account, it is estimated that demand will increase by about 2 million to 3 million tonnes by 2010.

Increased supplies could come from the reduction of discards and post-harvest losses. The increased utilization of small pelagics for direct human consumption could be another key issue for the region, but will need to be based on economic, technological and marketing feasibility. Regarding increased landings, commercially exploited marine species are generally in an advanced state of exploitation and existing stocks will need better management to meet future demand. In addition, fish production in the Latin America and the Caribbean region will fluctuate according to the variability in abundance of small pelagic stocks.

Current inland fisheries production trends will probably become more pronounced in the future. In the south - Argentina, Chile and parts of Brazil - trends to close fisheries to commercial exploitation and to reserve them for recreational and subsistence activities will continue. In the central part of the region, commercial fisheries on rivers and reservoirs will continue at generally low productivity levels. In the north, and in particular in the drought polygon of Brazil, in Cuba and Mexico, the intensified management of reservoirs through stocking and species introduction is expected to continue. Given these trends, increased production will be possible subject to careful management and the enhancement of Latin American reservoirs.

Export-oriented industrial aquaculture has expanded significantly in the region and still has moderate growth potential. Other types of aquaculture, such as pond-based fisheries in reservoirs, freshwater fish culture, mollusc and aquatic plants culture, have all grown less than expected. Regional aquaculture potential derives not only from available resources (water, land, coasts, temperature, agriculture, etc.) but also from the existing institutional set-up, research and entrepreneurial capacity. Most problems regarding the slow growth of aquaculture concern these factors. One important consequence is that socially oriented aquaculture as well as aquaculture oriented towards producing low-value products for low-income social sectors have developed little. A future challenge will be to institute measures that take advantage of the existing potential for these types of aquaculture production.

BOX 14

|

Fish-eating countries, particularly in the Caribbean, will continue to depend on fish imports although improved management of their resources and exploitation of large pelagics could bring some relief to the import bill. In parallel, other foods may replace fish to a certain extent.

Given the strong influence of international demand in terms of volume and unit value, and the orientation of the regional export industry towards foreign markets, the value of fish exports should continue to grow. One important condition is that macroeconomic and sector policies help keep regional products competitive. The trend of producing more value-added products rather than selling only raw material for the processing industries will probably continue in the coming years. Measures relating to trade and environment could generate economic problems for some sectors of the fishing industry as with the tuna-dolphin and shrimp-turtle issues.

1 This review is based on the regional study prepared by the FAO interdepartmental task force, headed by M. Lizarraga, Fishery Policy and Planning Division/International Institutions and Liaison Service (FIPL).

The region includes Canada, Greenland and the United States (excluding the Caribbean and the South Pacific islands but including Bermuda and Saint-Pierre-et-Miquelon as well as Alaska) and the adjacent fishing areas of the northwest and central Atlantic and the northeast Pacific. Owing to the structure of available data, the review is mainly concentrated on the situation in Canada and the United States.

With a total production of 7.1 million tonnes in 1994, the North American region contributes about 6 percent of global fish catch. Marine commercial landings have fluctuated somewhat during the last decade with catches from the north Atlantic decreasing. Aquaculture and recreational fisheries show a more steady growth. Food fish consumption averages a per caput supply of some 22 to 23 kg (live weight equivalent) annually and has been stable during the last few years. The United States in particular, but also Canada, is a major importer as well as an exporter of fish and fishery products. In Greenland, fish represents over 90 percent of the total export value of the island.

RESOURCES AND PRODUCTION

Marine fisheries

In 1994, total marine catches of the North American region were 6.5 million tonnes, representing a slight decrease in volume compared with 1993 but higher than in 1992. Production has been fluctuating after a steady upward trend over about 20 years up to 1990, when regional landings peaked at 7.2 million tonnes. The main reason behind the recent stagnation derives from the overexploitation of the principal commercial groundfish stocks in some areas where fisheries are now closed or subject to restrictions. For example, in the north Atlantic, cod, which used to contribute the majority of landings, is under moratorium off the northeast coast of Canada and, thus, attains only a small fraction of earlier production values. Furthermore, such restrictions have brought about socio-economic change in many communities in that area which depended completely on the marine harvest for their livelihoods.