![]()

![]()

![]()

W.E. Mabee

Warren Mabee is with the Faculty of Forestry, University of Toronto, Ontario, Canada.

This article examines current trends and their causes in wastepaper recovery and builds three scenarios for possible future developments.

Recovered fibre refers to any fibre that is recycled; that is to say, used more than once in the manufacture of a paper or a board product. By far the greatest volume of fibre recycling is that of paper and paperboard.

There is strong and growing pressure from public interest groups and governments to increase the recycling of wastepaper, and over the past ten years there have been great increases in the amounts of paper being recycled, driven by a combination of environmental and economic factors. Environmental organizations emphasize the conservation of natural resources; governments and local authorities are more concerned with finding alternative outlets for various components of solid waste, including wastepaper. These concerns have resulted in a number of legal and financial incentives for wastepaper recovery.

On the economic side of the equation is the actual and potential value of wastepaper as a raw material for the paper and paperboard industry, which currently absorbs the vast majority of all wastepaper that is reutilized. The economic advantages of wastepaper as a source of fibre in the paper industry include potentially reduced effluent discharges, as only slushing (as opposed to pulping and slushing from virgin fibre) is needed to disintegrate wastepaper into fibres; water consumption is reduced compared with that required for chemical pulping; and mechanical processing is reduced, leading to lower energy costs.

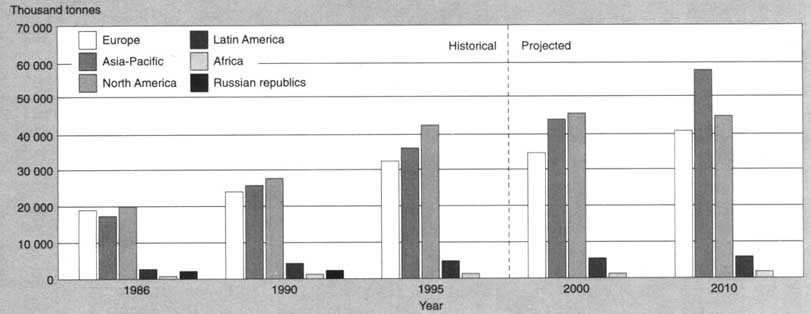

In preparing the paper on which this article is based, the author examined the historical production of paper and paperboard products for every paper-producing country. From the historical data (1986-1995), it can be seen that distinct trends emerge on a regional basis. In four regions (North America, Latin America, Europe and Asia-Pacific), overall wastepaper recovery rates increased by almost 10 percent. In Africa and the Russian republics, on the other hand, growth has been much less. Both of these regions have suffered from major political turmoil or have endured major natural disasters, which have made wastepaper collection and the accurate reporting of related data very difficult.

The resulting trends of paper and paperboard production were used as a baseline for three scenarios of wastepaper recovery. Two basic assumptions were used in the exercise:

ii

) In the event of a declining trend in the case of paper and paperboard production, it was assumed that the country's output would not fall beneath 10 percent of the highest reported national production level. This precludes predicting levels of zero production and reflects the fact that, if they are present, established mills in these countries would be likely to be used.

ii) Paper and board exports are also assumed not to go above 90 percent of the overall paper and hoard production. This is an artificial limit which is designed to restrict export levels to a realistic fraction of the total production.

Predicting the recovery of wastepaper in the future is obviously a difficult endeavour, given the number of variables involved. For every country, these variables include population, the level of development, the industrial capacity for wastepaper, the presence and condition of necessary infrastructure such as roads and the political and public opinions regarding the recycling of paper.

It is important to note that wastepaper recovery (the simple collection) is not the same as wastepaper utilization. The utilization of wastepaper requires large capital investments in mills and machinery (although these may be less than for plants based on the use of virgin fibre as a raw material), while wastepaper recovery can be achieved at a much lower cost. In fact, as a result of pressure from an environmentally sensitive public in industrialized countries, there has been a tendency to develop recycling programmes before the capacity to utilize the wastepaper is established. Therefore, not all wastepaper being recovered is necessarily being put to use. Other works on this subject attempt to establish levels of recovery and utilization (FAO, 1992; 1994). In this article, the emphasis is on recovery and the theoretical amounts of paper available from this recovery.

Figure 1 shows the wastepaper recovery rates for the past decade, based on published figures from around the world (Chandler, 1990; 1992; 1994; 1996). If, as a starting point for discussion, historical trends are extended into the future, it can be seen that four of the six regions North America, Europe, Africa and Asia-Pacific - will experience more increases in wastepaper recovery while Latin America will maintain its current level of recovery and that of the Russian republics will remain low.

FIGURE 1 - Wastepaper recovery by region, historical and projected data, 1986-2010

Scenario 1: projected wastepaper recovery

The first scenario for wastepaper recovery is based on a projection of the historical data to the year 2010. This was done by conducting linear regressions on published production data and then projecting the resulting trends into the next millennium. In making these projections, one must make two additional assumptions to prevent the trends from becoming unrealistic:

i

) Wastepaper recovery cannot fall beneath 10 percent of the highest reported recovery level or above 100 percent of [P&B Production+Imports+Exports], whichever is lower.

ii) If there are no reported values for paper and hoard production or wastepaper recovery after 1990, then production and recovery is assumed to have stopped and zero is used.

This scenario has the limitation of not differentiating between highly industrialized and developing countries, which may experience radically different changes in wastepaper recovery over the next 20 years. Nor does it make any allowances for natural disasters or political upheavals, both of which could drastically affect the industrial output of individual countries. The results of this projection are shown in Figure 2.

FIGURE 2 - Wastepaper recovery levels by region - Scenario 1

By 2010, North America's projected recovery rate of 68 percent would be higher than any of the other regions. The European recovery rate would be approximately 56 percent, which is far below the regions stated and assumed goal of 90 percent recovery. Both North America and Africa would show significant gains in recovery rates (+23 and +13 percent, respectively), while Europe would experience a moderate increase (+9 percent). The Asia-Pacific and Latin American regions are projected to be stagnant and the Russian republics would experience a significant decline in wastepaper recovery if current trends continue. However, should the countries comprising the latter region enter a period of relative political stability, large increases could be expected in both paper production and paper recycling.

Scenario 2: optimal wastepaper recovery

This scenario is that of an ideal world, in which goals and targets for wastepaper recovery would be met by every country on the planet and high levels of recycling would be possible. In determining a wastepaper recovery target for each region, figures were chosen based on current recycling levels in each of the six global regions and on previous predictions of growth. For instance, Europe, being a compact, highly developed area with traditionally high levels of recycling, was given a target of 90 percent wastepaper recovery. This figure reflects that published in FAO market reviews (FAO, 1992; 1994).This figure is also indicative of a theoretical maximum for recycling, as it is unlikely that levels of much greater than 90 percent wastepaper recovery could be reached in the real world. Other ideal levels were based on estimates of the potential best recovery that a region could expect in the time period allotted. The goals set for the other regions were: Asia-Pacific, 75 percent recovery; North America, 75 percent; Latin America, 50 percent; Africa, 50 percent; and the Russian republics, 40 percent. It should be noted that the target levels given here probably exceed realistic goals for wastepaper recovery. Instead, this scenario should be treated as an analysis of theoretical maximums.

It can be seen from Figure 3 that, under Scenario 2, almost 300000 tonnes of wastepaper (total) would be recovered in 2010. This is almost five times the amount of collected wastepaper available as of 1986. Of all the regions, the greatest increase in recovery levels and rates would take place in the Asia-Pacific region, which currently relies heavily on imports of recovered paper from North America to meet recycling quotas. North America, Europe and Latin America would also have to improve recovery rates significantly to meet the desired goals.

FIGURE 3 - Wastepaper recovery levels region - Scenario 2

Scenario 3: minimal wastepaper recovery

The third scenario makes an initial assumption that no further advances will be made in wastepaper recovery. An analysis of the historical data shows that this has happened in the past in some countries. Under this scenario, although recovery levels as a percentage of production would remain constant at their 1995 levels, the absolute amount of wastepaper being recovered would rise as a factor of overall paper and paperboard production. In Figure 4, the wastepaper recovery levels are illustrated. Even under these conditions, however, the Asia-Pacific region would become the most active region in terms of paper recycling. The sheer projected volume of paper and paperboard production in this region means that even low levels of recovery would yield large amounts of wastepaper.

FIGURE 4 - Wastepaper recovery levels by region - Scenario 3

The North American and European regions could show significant gains in recovery levels as well, owing to the continual growth that the pulp and paper sectors in these regions may experience.

The historical and future trends in wastepaper recovery, as well as total paper consumption, are displayed in Figure 5. Paper consumption is expected to rise by about 35 percent over the next 20 years, peaking at about 39000000 tonnes. The recovery of wastepaper is expected to range from 42 to 77 percent of the overall consumption figure. The current trends in wastepaper recovery should bring us to approximately 50 percent of the amount of paper consumed by the year 2010.

The world's recovered wastepaper supply has historically been dominated by three regions: Europe, North America and Asia-Pacific. The scenarios described above indicate that this trend continue into the future. The Asia-Pacific region in particular is poised to become the world's leader in wastepaper recovery. The combination of a large, educated population in many countries in this region, together with a pulp and paper industry that is growing strongly, will provide the impetus for rapid increases in the recovery of wastepaper. Under both the second and third scenarios, the region will become the leader in wastepaper recovery, in terms of total tonnes collected, by the year 2010. Even assuming a continuation of current trends in recovery rates (Scenario 1), the region would supersede Europe by a some 10 million tonnes of recovered wastepaper per year.

The North American and European regions will continue to recover large amounts of wastepaper in the future. If current trends continue, North America will recover the largest amounts of wastepaper, followed by the Asia-Pacific region and then Europe. Under scenarios 2 and 3, North America would lose its top position in wastepaper recovery. Under all three scenarios, the European traction of the total world's wastepaper recovery will decline in future years, reflecting the stability of this region in comparison with other parts of the globe.

The two most important regions in terms of global trade in wastepaper will continue to be North America and the Asia-Pacific region. As stated above, the growth in Asia-Pacific can only mean increases in the amounts of wastepaper recovered. However, as shown in Figure 6, there will be a shortfall between wastepaper recovery and consumption that can only be expected to grow. The surplus wastepaper that North America can supply, while currently more than adequate to meet the Asia-Pacific region shortfall, will not be able to keep up with rising demand in the future.

FIGURE 6 - Not wastepaper recovery by region, 1986-2010

The reliance of the Asia-Pacific region on North American wastepaper could prove to be a problem in future years. It can be assumed that, with extensive growth in this region, the demand for wastepaper will continue to rise, possibly outstripping the supply that North America can offer. Should this happen, wastepaper recovery will have to rise greatly in the Asia-Pacific region in order to meet demand. This could have major effects on the overall price of wastepaper in this region and may lead to large capital expenditures within the region for the establishment of paper recovery and recycling facilities.

The other four world regions seem to be consuming more wastepaper than they are recovering. There is a large world market for wastepaper. Europe, Africa, Latin America and the Russian republics each have a low level of demand that probably could be served through reserves of wastepaper from more prosperous years, or from interregional trade taking advantage of differing national recovery levels in the member countries of these regions.

Latin America seems most likely to contribute to the world supply in the years to come. Africa and the Russian republics, owing to political instability and lack of development, will not recover large amounts of wastepaper in the foreseeable future. This is largely due to the lack of a well-developed pulp and paper industry and the absence of the infrastructure necessary to collect and recover wood fibres.

Chandler, W.V. 1988. PPI Annual Review. PPI, 30(7): 46-129.

Chandler, W.V. 1990. PPI Annual Review. PPI, 32(7): 43-144.

Chandler, W.V. 1992. PPI Annual Review. PPI, 34(7): 32-122.

Chandler, W.V. 1993. Material recycling: the virtue of necessity. Tappi J., 76(9): 82-87.

Chandler, W.V. 1994. PPI Annual Review. PPI, 36(7): 17-102.

Chandler, W.V. 1996. PPI Annual Review. PPI, 38(7): 22-95.

FAO. 1992. Annual Forest Products Market Review 1991-1992. Timber Bull., XLV(3): 38-39.

FAO. 1994. Forest Products Annual Market Review 1993- 1994. Timber Bull., XLVII(3): 19-25.

Guest, D. 1996. The great wastepaper mystery. PPI, 38(4): 72.

Hagler, R.W. 1995. The global wood fibre balance: what it is, what it means. Proc. Tappi Global Fibre Supply Symposium, p 119-125. Atlanta, USA, Tappi Press.

Kenny, J. 1996. Watching the world get smaller. PPI, 38(8): 48.

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}