FERTILIZERS

UREA

|

|

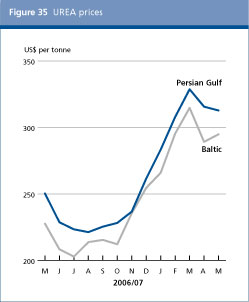

The strengthening in Urea prices continued in May 2007, largely in response to India procuring about one third of its expected annual import requirements. The seasonal slow down in demand in the United States and in Europe, however, could dampen further price pressure which could be brought about by additional import demand from India and from countries situated in Latin America. The persistence in high prices generally reflects tighter markets, partly resulting from increasing fertilizer applications to grain crops in response to rapidly expanding bio-fuel production in the United States. In that country, urea purchases are sourced from Canada, China, Egypt, Venezuela and Saudi Arabia. In Indonesia, urea application has been affected by adverse weather conditions which could prompt increased international purchases by the country. Demand in China is expected to strengthen in anticipation of summer plantings. Ample supplies in Pakistan could see the country exporting in the near horizon.

DIAMMONIUM PHOSPHATE (DAP)

|

|

Sustained growth of demand for diammonium phosphate (DAP) in the wake of supply constraints, suggest higher prices in the near future. Import demand for Diammonium Phosphate (DAP) is currently limited to India, while Pakistan and countries in Latin America may enter the international market at a later stage. Moroccan phosphate exports, except Mono ammonium phosphate (MAP), have recorded fast growth. In the United States, DAP production and exports marginally declined while both rose in the case of MAP. Short-term prospects for export availabilities have deteriorated following Chinas imposition of a 20 percent export duty on selected phosphate products. In Europe and the United States, manufacturing of compounds and stock replenishing for fall plantings are being undertaken. In Pakistan, DAP demand surged by about 50 percent from 2006 in response to the implementation of a revised fertilizer subsidy policy, which is scheduled for review in mid-2007. In Vietnam, DAP is reportedly in short supply and further imports are scheduled. DAP availability in Brazil and Argentina is sufficient for the time being, but demand could rise as the season progresses.

MURIATE OF POTASH (MOP)

|

|

Muriate of Potash (MOP) prices have generally remained firm over the last two years, and rising demand in Asian markets from North America could pave the way for further price increases. Imports by China increased by one-third. Exports from Russia, Belorussia and Israel have risen owing to strong MOP demand in Brazil. In Europe, potash suppliers were reported to be heavily committed, with low stocks remaining to meet unexpected demand. In North America, potash production and exports increased and inventories have been reduced. The MOP market situation in the Russian Federation is buoyant, as domestic demand shows high growth. Continued tight supplies in the United States and the need to meet large import requirements from India could prompt further MOP prices increases in the near future.

| |

March 2007 |

April 2007 |

April 2006 |

Change

from last

year 1 | | | | | | |

US$ per tonne |

Percentage | |

UREA | | | | | | | | | Baltic | 311 | 319 | 284 | 295 | 247 | 250 | 26.6 | | Persian Gulf | 325 | 333 | 312 | 320 | 258 | 262 | 26.6 | |

AMMONIUM SULPHATE | | | | | | | | | Eastern Europe | 130 | 135 | 131 | 136 | 80 | 83 | 63.4 | |

DIAMMONIUM PHOSPHATE | | | | | | | | | North Africa | 379 | 386 | 423 | 431 | 252 | 263 | 48.4 | | US Gulf | 410 | 415 | 432 | 435 | 259 | 263 | 58.3 | |

TRIPLE SUPERPHOSPHATE | | | | | | | | | North Africa | 265 | 267 | 310 | 316 | 176 | 183 | 48.5 | |

MURIATE OF POTASH | | | | | | | | | Baltic | 165 | 178 | 165 | 177 | 130 | 151 | 22.1 | | Vancouver | 171 | 184 | 174 | 182 | 130 | 155 | 24.4 |

Source: Compiled from Fertilizer Week and Fertilizer Market Bulletin.

1 From mid-point of given ranges.

|

June 2007

June 2007