|

|

SPECIAL FEATURES

Falling prices in perspective

|

|

Prices for most agricultural commodities have dropped significantly and swiftly in recent months. World grain prices have fallen by over 50 percent from their record highs earlier this year. International prices for other important foodstuffs, such as vegetable oils, oilseeds or dairy products have also drifted downwards, even if they still remain above their longer term trend levels. Rice is still expensive but prices may follow the path for other foodstuffs as the new crop comes on stream, export restrictions are relaxed and demand shifts further to cheaper alternatives.

At first sight, this is good news for the global food system. But the gradual return to equilibrium in food markets should not be taken to assume that the worlds food problems have been fixed, neither in the short-run nor with a view to the longer-term challenges. Cereal stocks still need to be replenished and lower prices will again divert more supply from food to fuel. With only 433million tonnes in opening stocks, the cereal stocks-to-use ratio in 2008/09 is at its second lowest in three decades. To bring stocks back to their pre-crisis levels will require 40percent of the production increase in 2008. Bioenergy has already absorbed 100million tonnes of cereals in 2007/08. Falling feedstock prices and new bio-ethanol production capacities arriving, could stimulate new demand and thus moderate an otherwise more drastic decline in prices.

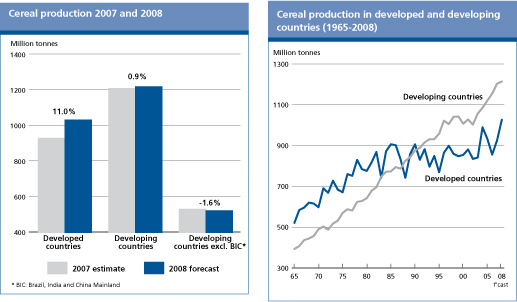

The recent decline in prices should neither be taken to mean that the worlds problems of hunger and poverty have been solved. A casual glance at the most recent production statistics reveals that most of the production increase of the last two years arose in developed countries. The benefits of higher prices have not accrued to producers in many developing countries, for their supply response was small in 2007 and virtually zero in 2008 (see figures). The reasons are manifold. Higher prices of key agricultural inputs such as fertilizers, seeds and energy, made it more difficult for all farmers to step up production. But particularly hard hit were poor subsistence producers who have been confronted with higher input prices without producing a marketable surplus that would earn them higher revenues. At the same time, export taxes and restrictions meant that high international prices were not always and not fully transmitted to domestic markets, burdening even commercial farmers with higher costs and stagnant output prices. The policy response to soaring food prices in developing countries was indeed wide-ranging. A FAO survey found that nearly 40 countries reduced grain import tariffs and more than 20 countries imposed export controls of some kind either in the form of taxes or quantitative controls such as outright bans and quotas.

Even more worrisome is the notion that falling prices have little to do with recovering global supplies but instead are being driven downwards by slowing demand. This is being evidenced by the fact that almost all commodity prices are declining in unison alongside a deteriorating global economic outlook. The entrenchment of the global financial crisis could mean that the economic slump may even be faster and more severe than currently anticipated. To the extent prices do reflect an anticipated slow-down in economic growth that constricts demand, lower prices may even be associated with more poverty and hunger rather than less.

And finally, the recent decline in world food prices should not be taken to conclude that the fundamental, longer-term issues have become irrelevant. Land and water constraints remain for the most part unaddressed, investments in rural infrastructure and agricultural research are still low, agricultural inputs remain expensive relative to farm-gate prices, and the need to adapt to climate change is more urgent than ever before. It is therefore important to seize this window of opportunity to reflect on how to avoid subsequent crises by addressing the longer-term challenges. Without trying to provide a complete account of them, some of the most important challenges are the following:

World population is projected to grow from 6.5 billion in 2005 to nearly 9.2 billion by 2050. To feed a population of more than 9 billion free from hunger, global food production must nearly double by 2050. The entire population growth will take place in developing countries and it will occur wholly in urban areas, which will swell by 3.2 billion people as rural populations contract. That means that a shrinking rural work force will have to be much more productive and deliver more output from fewer resources. Higher productivity requires more investment in agriculture, more machinery, more implements, tractors, water pumps, combine harvesters, etc., as well as more skilled and better-trained farmers and better functioning supply chains.

Fewer farmers will have to feed a more populous world with fewer resources. One way would be for world agriculture to expand its land basis and use some of the nearly 4.2 billion hectares potentially available for rainfed crop production (only 1.5 billion ha are currently in use). But that would not be possible without further environmental damage and increased greenhouse gas emission. Another avenue would be to tap into yet-unused yield-enhancing resources, which could double productivity for many crops in many countries. However, such potential can only be realized if farmers have improved access to inputs, apply better fertilizers in more abundance, make use of better seeds, improve their farming and management skills and expand land under irrigation.

-

In addition to rising resource scarcity, global agriculture will have to cope with the burden of climate change. The IPCC has documented the likely impact of climate change on agriculture in great detail. If temperatures rise by more than 2oC, global food production potential is expected to contract severely and yields of major crops may fall globally. The declines will be particularly pronounced in lower-latitude regions. In Africa, Asia and Latin America, for instance, yields could decline by 20-40percent. In addition, severe weather occurrences such as droughts and floods are likely to intensify and cause greater crop and livestock losses.

-

Rapidly rising energy prices have created an added challenge for global food supplies. Rising fossil energy prices mean that agriculture will become increasingly important as a supplier to the energy market. Important here is to understand that the potential demand from the energy market is so large that it has the potential to change the worlds traditional agricultural market systems completely.

These challenges can only be mastered if both private and public hands start investing in agriculture now. The FAO has tabled an investment road map to 2015 and gauged its potential benefits. This assessment suggests that a total annual investment volume of USD 30 billion in the following five areas would engender an overall annual benefit of USD 120 billion.

1. Improve agricultural productivity and enhance livelihoods and food security in poor rural communities.

2. Develop and conserve natural resources.

3. Expand and improve rural infrastructure and broaden market access.

4. Strengthen capacity for knowledge generation and dissemination.

5. Ensure access to food for the most needy through safety nets and other direct assistance.

Agricultural Commodity Markets and the financial crisis

|

|

According to the IMF World Economic Outlook published on 9 October 2008, the world economy is set for a major downturn triggered by what it describes as the most dangerous financial shock since the1930s. The IMF has revised its growth forecasts sharply downwards accordingly, to only three percent in 2009 as a slow down is expected in all the major economies.The three percent global growth figure would be largely sustained by continuing high growth rates in India (6.9 percent) and China (9.3 percent). The IMF expects some recovery after 2009, but this will be unusually gradual and depend on the impact of the various rescue measures introduced. Other commentators are more pessimistic, talking in term of years of sluggish growth.

The financial crisis follows hard on the heels of the soaring food prices episode and will obviously have implications for international agricultural markets and the agricultural sectors of developing countries. Agricultural commodity prices have been falling for some time now, following oil prices downwards and, amongst commodities in general, only gold prices are holding up. The final impact of the crisis on commodity prices is, at this stage, difficult to assess as the various forces at play impinge on prices in opposite directions. A discussion on the possible channels through which the crisis could feed into commodity markets could nonetheless help identify the key factors to be closely monitored.

The impacts of the financial crisis will be felt in developing countries at the macro-level, with potentially negative effects on their agriculture sector and on their food security. The channels through which agricultural markets will be affected are on both the demand and supply sides.In general, the slowing down of economic growth would affect international demand for commodities, especially raw materials and livestock products, negatively, with such impact likely to be more limited for staples such as rice. Apart from the direct impact of slower rates of GDP growth, the prevailing uncertainty and consequent negative market expectations could further dampen demand. If, as is sometimes claimed, demand from China and India and other rapidly growing economies in the developing world has a dominant impact on the world agricultural commodity demand and prices, then the anticipated continued high growth rates in these two countries may help contain the negative impact of falling world income growth on agricultural commodity markets. However, overall, the result of falling demand is likely to be further downward pressure on agricultural prices. The recent drop of oil prices may also depress the demand for those commodities usable as feedstock in biofuel production, although this will depend upon the relative movements between oil and feedstock prices. In general, lower food prices are good news for consumers, but suppresses incentives for producers to make the investments necessary and desirable to secure greater food security in the medium term. In addition, thedrop of food prices benefiting consumers would probably not be sufficiently to compensate them for declining household incomes in the event of a worldwide recession, as economic activity slows, employment falls and remittances from abroad dry up.

On the supply side of commodity markets, the reduction of price incentives is likely to result in some cutback in agricultural production. However, the impact of the financial crisis on incentives depends on more than just product prices. In particular, the financial crisis may also depress input prices, especially if energy prices continue to weaken, as this could also trigger a reduction in fertiliser and all energy-related costs, from production, to processing, to transportation - freight rates have also halved in the past few weeks -. The net effect on production will depend upon the relative speed of adjustment of output and input prices. It is possible that the input prices will be more sticky and fall at a slower pace than product prices, in which case producer margins will be squeezed further. However, even more critical is likely to be the impact of the financial crisis on the availability of credit, which is widely recognized as one of the major constraints to agriculture development in the developing countries, the rationing of which is likely to be more serious than any interest rate effects. The combination of falling agricultural prices and reduced access to credit may have a knock off impact on agricultural production, with very serious implications for the global food security.For instance, a cutback in grain plantings against the background of continuing low grain stocks, which have not been rebuilt since the high food price episode, would increase the risk of global food crisis if harvests turn out to be poor, especially if countries cannot access credit for food imports.

The extent of the impact of the global credit crunch on the financial position of developing countries will depend not only upon the implications for their economic growth rates but also upon their borrowing situation and dependence upon international credit and transfers to finance food imports and agricultural development. Estimating these impacts will need an assessment of the importance of external funds, whether government-to-government borrowing, bank lending, official development aid, foreign direct investment and remittances. All may be compromised by a deepening financial crisis. In this regard, it will be particularly important that donor countries and investors meet their commitments taken towards the development of agriculture in the developing countries, especially at a time when agriculture may, as appears to have been the case over the 1996 Asian financial crisis, act as a buffer and help cushion greater losses incurred in other sectors of the economy. Besides the possibility that governments reassess downwards their commitments to international development aid, there is also a risk that the great uncertainty now surrounding international markets and the threat of global recession tempt countries towards protectionism. It would be unfortunate if this were to be the case and if the recently mobilised political will towards enhanced international support for developing country agriculture was to fade away.

|

November 2008

November 2008