![]()

![]()

![]()

What does the future hold?

FAO global outlook study, 1996

Selected policy-related implications

One of the most pressing questions regarding the future outlook for the sector is whether there is enough wood to meet expected demand. To work towards a clearer view of the future, in 1996 FAO commissioned an updating of its global outlook projections on forest products to the year 2010.1 The provisional results are released in this report with final authoritative figures to be issued in 1997.2 Present indications are that, at least until 2010, there will be adequate wood globally to meet both industrial and fuelwood needs, although local level shortages will exist simultaneously with surpluses elsewhere.

1 FAO Provisional outlook for global forest products consumption, production and trade. 1997. FAO Forestry Department, Policy and Planning Division, Rome, 1996. Prepared by Dali Zhang, Buongiorno, J., Rytkonen, A., Zhang, Y, and Zhu., S. Antti Rytkonen (Finland) was FAO consultant; the other team members are all affiliated with the Department of Forestry, University of Wisconsin at Madison, USA.2 FAO's views are provisional while awaiting finalization of the global outlook study on forest products and completion of its Global Fibre Supply Study (see Box 1).

The opinion of many recent analyses is that a real long-term increase in prices is unlikely or would, on the world scale, be far less than expected if supplies became critically short. There continues to be a need for prudent management of forest resources and an improvement in consumption behaviour. A much better future would be possible if efforts are strengthened to create new forests or to improve management of existing ones. Also, more wide-scale adoption of use of residues and recycling in forest industries, as well as less wasteful use of forest products, would be most beneficial. Addressing major fuelwood deficits will require particularly vigorous efforts.

Assuming continuation or improvement of free-trade regimes in the post-Uruguay Round era, trade should be able to match regional and national deficits for industrial products with supplies from elsewhere, even for most developing countries. These countries as a group have been playing an increasingly important role in global trade, and trends suggest they will play an even larger role in the future. However, many developing countries lack the capacity to participate adequately in trade and these will require national solutions to meet their needs. Even now, there are severe local shortages of supplies which, in the case of non-traded materials like fuelwood, cannot be corrected through the international marketplace. For these types of products, local actions will be essential to avert hardship.

A potentially tight, but not crisis, softwood supply situation is expected in North America until plantations in the southern USA and the Pacific Northwest mature. In the meantime, greater use of hardwoods can, if consumer tastes permit, ease the tight situation, and shortages in the USA could be met by imports from Canada; this would represent only a modest change in the substantial trade between the two countries. More efficient use of raw material through further technological and recycling improvements can also help, although further gains in yield will be less easy to capture than in the past. In Europe, forest growth will continue to exceed removals and further efficiency improvements are likely.

Major deficits in Asia will pose the greatest challenges. Asia's consumption of many industrial forest products already equals or exceeds that of Europe. The growth in demand is projected to outstrip supply potential for almost all products, leading to fast growth in imports. Some dislocation may occur, but trade with regions such as the former USSR, Oceania and the Americas, and increasing supplies from its own plantation resources are likely to be able to accommodate this. It is significant that Asia's consumption is dominated by countries pursuing free trade regimes, and whose reciprocal open-door trading relationships should permit international supplies to contain the situation at least until 2010.

In its revised projections, FAO has assumed that there will be no major policy changes regarding the relative importance and attention given to wood and non-wood functions in forest management. In recent years, calls for 'ecosystem management', which respects multiple purposes and functions of forests, have been supplemented or supplanted by calls for forest preservation which would exclude the harvesting of wood. Timber supplies from US public lands have already been reduced significantly; a recent study for North America (see Box 2) estimates that adoption of 'ecosystem management' has helped to reduce annual timber supplies from Federal lands in the USA from about 50 million m3 to less than 20 million m3.

The issue is whether the trend towards preservation-oriented forestry will continue and whether it will transform the policies of key producer countries, particularly in North America, Europe and Asia, causing them to restrict harvesting over large areas of production forests. This may also apply to South American forest resources; an additional potential brake on world flow of forest products would occur if large areas of natural forests in South America, the subject of much international scrutiny, become inaccessible (for policy reasons) as a source of industrial forest products. Recognizing society's growing preoccupation with environmental matters, the recent UN-ECE/FAO fifth European Timber Trends Study considered, among others, the possibility of a 'deep green' future. This was considered unlikely in Europe but, if it occurred elsewhere, a major reassessment of the outlook situation would be required. The severe restrictions on availability of wood that could ensue would cause significant real price increases for forest products and thus encourage displacement of wood products in the marketplace by substitute materials.

Adoption of deep-green or similar policies is only one factor that could affect availability of forest resources for industrial utilization. Another important factor is economic accessibility. Recently, internal transport tariff charges and railway developments in the Russia have made transport of timber out of Siberia uneconomic. Many large forest areas in both Africa and South America are also physically and economically inaccessible, a situation which may not change significantly in the decade and a half ahead. On the other hand, the availability of wood from plantations is increasing rapidly in Oceania (particularly New Zealand) and South America and will eventually do so in the southern USA.

In the pulp and paper field, any shortages or restrictions to access of forest raw materials might tend to encourage greater use of non-wood fibre. In the Asia region, industry based on non-wood fibres is already significant and can expand beyond China and India, which now account for practically all the existing capacity. The transport economics of using non-forest fibres, such as straw, militate against large mills. A consequence would therefore be perpetuation of small pulpmills unable to afford pollution abatement technology. The already well-known pollution problems of this sector, caused by small-scale operation, would then worsen. Policies need to recognize and respond to the fact that, in attempting to preserve forests for environmental reasons, the pulp and paper industry may be driven to greater reliance on a polluting non-wood based alternative which could damage the environment even more. However, the recent closure of many small paper mills in China appears to indicate a willingness to import rather than to incur environmental costs.3

3 AP news Beijing, 23 October 1996 reported that 'nearly 50 000 small paper mills and other factories that caused heavy pollution' had been closed.

The long-standing concentration of consumption and production of forest products (both in regional terms and with respect to countries within a region) is expected to continue. Concentration of supply of forest products demands a closer look. World industrial forest products economy is geographically-dominated mainly by three areas - North America, Asia and Europe - which already account for around 80 percent of world production of roundwood and sawnwood, and more than 90 percent of panel products, and pulp and paper commodities. The Pacific Basin countries in Asia, the Americas and Oceania, account for some two-thirds of world consumption of forest products, with Asia increasingly approaching North America in total demand, and South America's demand for industrial roundwood being about one-half of that of Asia. This situation places the forest resources of Pacific basin countries, including those of the Russian Far East and South America, at the front line of the world supply/demand equation in the foreseeable future North America, Asia and Europe, the three leading geographical regions in terms of wood and fibre supply, together with the former USSR, include the whole of the northern temperate and boreal forests. With continuing industrial utilization and settlement, the original vegetation in accessible locations has been reduced dramatically, although large inaccessible expanses of Siberian and north Canadian boreal forests remain untouched. Public and interest-group pressure to conserve what remains by including more of it in protected area systems and/or to change management practices has increased.

This raises a number of unanswered questions. What will be the extent and impact of such pressure? Will it result in restrictions on industrial use of temperate and boreal forests over extensive areas? If so, would tropical forests become a more important source of supply? There have already been claims by some environmental groups that consumers in industrialized countries are 'exporting deforestation' to developing countries by consuming tropical forest products. Shall we see this kind of campaign escalate? There are no indications that this will happen on a major scale but local situations can affect supply/demand balance in specific countries.

|

Box 1 A number of studies have been carried out in recent years, some of which were the result of private sector concern over the projections issued by FAO in 1991 and 1995. The studies provide a variety of views on adequacy of supply relative to expected demand. For example, in 1995, Jaakko Pöyry Consulting published assessments of the global fibre situation and concluded that there is ample wood fibre available on a global basis.4 In the same year, Sedjo and Lyon, using an equilibrium approach, predicted that wood supply and demand would increase at nearly comparable rates but foresaw the composition of industrial roundwood production shifting towards smaller logs due to greater importance of paper/paperboard and composite panels in future forest products consumption.5 Apsey and Reed, in 1995, while recognizing that actual consumption must necessarily equal production, projected that demand would exceed availability on a global scale by a 'hypothetical gap' of some 400 million m3 in 2010, and nearly 600 million m3 in 2020, implying price increases.6 A year later, Nilsson had, as his 'mainstream' result, a situation whereby potential demand would exceed supply by nearly 800 million m3 in 2010 and nearly 900 million m3 in 2020.7 Solberg et al., however, concluded that the world's forests are capable of providing industrial wood consistent with consumption projections of the future.8 Most projections of future adequacy of supply fall within the same orders of magnitude, but a few project major supply gaps. Consensus appears to be tending towards a 'non-crisis' future situation. However, no study foresees plentiful supplies. A fuller analysis of the resources situation and its prospects will be available upon completion in late 1997 of the FAO Global Fibre Supply Study9, which was initiated following industry requests 4 Jaakko Pöyry. 1995. Solid wood products competitiveness study document. American Forest and Paper Association. Washington D.C.; and The Jaakko Poyry Group. 1995, Global fibre resources situation: the challenges for the 19 90s. Tarrytown, New York 5 Sedjo, Roger A. and Lyon, Kenneth S. 1995. A global pulpwood supply model and some implications. Final report to IIED; Resources for the Future, Washington, D.C. (Earlier, also published: Sedjo, Roger A. and Lyon, Kenneth S. 1990. The long-term adequacy of world timber supply In Resources for the Future. Washington D.C. 6 Apsey, Mike; Reed, Les. 1995. World timber resources outlook, current perceptions: a discussion paper. Second edition. Council of Forest Industries. Vancouver, BC, Canada; 7 Nilsson, Sten 1996. Do we have enough forests? International Institute for Applied Systems Analysis. Laxenburg, Austria. 8 Solberg, B. et al. 1996. Long-term trends and prospects in world supply and demand for wood and implications for sustainable forest management: a synthesis. European Forest Institute and Norwegian Forest Research Institute. Joensuu, Finland. A related detailed paper is: Brooks, D. et al. (in press). Long-term trends and prospects in world supply and demand for wood. In Solberg, B. (ed.), Long-term trends and prospects in world supply and demand for wood and implications for sustainable management, Research Report 6, European Forest Institute. Joensuu, Finland. 9 This study Is considering fibre supplies from all forest types and will construct three supply scenarios. Raw material for solid wood products as well as pulp and paper industries will be included; non-wood pulp and recovered waste paper will also be analysed. |

This section presents in more detail the results presented above of FAO's global projections to 2010 of forest products. The recent surge in outlook activity (see Box 1), of which these revised FAO projections are part, reflects the unprecedented interest in the fate of forests which has accompanied the UNCED process. FAO issued global projections in 1991 and 1995.10 Soon afterwards, it commissioned an evaluation of the forecasts, which revealed some methodological weaknesses and a tendency for results to be too high, partly due to over-optimistic assumptions of economic growth. A substantive updating of the projections system and a second look at the assumptions resulted in the set of provisional projections released for the first time in this report. The projections have the horizon year of 2010 and three scenarios, of which only the results of the 'most probable' scenario for the main commodities at regional level are given in this chapter. FAO plans a review process for the outlook study culminating in an international expert meeting. Official figures will be published in 1997.

10 Forestry statistics today for tomorrow, 1945-93; 2010. FAO. Rome, 1995. The 1995 release was an update of the earlier Forest products - world outlook projections (projections of consumption and production of wood-based products to 2010). FAO Forestry Paper No. 84, Rome 1991.

Key assumptions

The FAO study analyses the possibilities for equilibrium between demand and supply, taking into account all principal driving forces and constraints.11 At global level, consumption and production are always the same, apart from small annual variations attributable to changes in commodity stock between production and the market.

11 The full document should be consulted as a basis for understanding the results.

The study took particular account of population, income, prices and the availability of forest resources. Technological change was seen as an important consideration in view of evidence that it plays a key role in responding to changing supply situations. Economic growth was represented by GDP in constant 1987 US dollars with demand equations developed according to income groups. The income elasticities of demand were broadly matched to the income categories of countries. Specific constraints to the timber supply potential of each country were introduced, with the projected demand for wood as a raw material not being allowed to exceed the wood growing potential. In the absence of solid data for many countries, supply limits had to rely upon informed judgement. In total, the growth rate of world roundwood supply potential for the most probable scenario was calculated as 1.12 percent annually.

Other assumptions governing the projections were as follows: (a) capacity changes were based on past production, estimated new investments and the profitability of production; (b) technology was defined by input-output coefficients - held constant at the 1994 level, except for paper and paperboard; (c) fibre input mix assumptions were made, with substantial change expected by 2010; (d) inertia constraints to limit trade change in a given year (within 5-15 percent for the 'most probable' scenario) were introduced, given that adjustment of trade flows takes time; and (e) historical price trends suggested that the real price of industrial roundwood could peak initially but return to around the 1994 level in 2010 as price elasticities were observed to be generally low.

The projections

Indicative consumption levels for the 'most probable' scenario are presented in Table 1. Table 2 summarizes expected trade developments. The data are given at regional level for the major commodity groups. The complete set of data from the outlook study, which will be published in 1997, includes projections for sub-commodities, and for production and trade at country level. The Figures on pages 85 to 90 illustrate selected production and trade trends and prospects; for net trade the 'most probable' scenario is shown alongside two alternatives.

Table 1 - FAO 1996 provisional regional-level projections for consumption to year 2000 and 2010

Table 2 - FAO 1996 provisional projections of trade to year 2000 and 2010

Like all projections, these provisional projections and the data used should be considered in context and with caution, particularly with regard to: (a) the weakness of information on fuelwood, for which formal statistics are rarely collected; and (b) the severe disruption since 1990 of all historical trends for the former USSR, formerly a major producer and consumer of industrial forest products. The speed of its recovery is difficult to predict, as change will depend on policy developments well outside the control of either forestry or manufacturing sectors.

Significant growth can be expected for all commodities except sawnwood which is likely to maintain its slow growth. Exceptionally fast growth (near or more than 7 percent annually) has been recorded in the past for panel products, paper and paperboard, for pulp and for recovered paper for recycling. The future is likely to hold less rapid but still high growth rates of more than 4 percent for these products.

The greater use of recovered paper for recycling continues a trend which has already contributed to savings on primary raw materials. The FAO study did not analyse future trends in use of forest residues and mill wastes which can also significantly reduce demand for forest harvest. As more fibre is recycled or more residues used in manufacturing, fewer trees need to be cut for a given level of production. Europe is closer to the limits of recycling than North America and the other regions. The trade in waste paper will remain dominated by cross-Pacific exports from North America to Asia.

North America, Asia and Europe will consolidate their dominance in forest products. Within this group, Asia will increase its share of consumption and production. A number of figures in this chapter illustrate this situation for specific commodities. Demand is driven largely by income in all three regions (i.e., by the existing high incomes in North America and Europe, and the rapidly-growing incomes in the case of Asia) but, in Asia, it is also driven by rapid population increases. In a number of cases, Asia has already surpassed Europe (for industrial roundwood, fibre, paper and board) and the margin will grow with Asia's greater consumption beginning to approach or exceed North America's significance for some products. Furthermore:

· North America's broad ability to meet all its own forest products needs will remain unchanged. The surpluses of this region, although not large relative to internal consumption, will remain important for helping to fill the deficits of other regions, notably Asia.· Asia, despite the world's fastest increases in local production, will see its trade deficits grow even further. Even for veneers and plywood where it still enjoys a surplus, Asia is expected to turn to shortfall soon after the turn of the century. Also pulp and paper, where Asian investments regularly make headlines in the industry press, the shortfalls will continue to worsen.

· In terms of demand/supply balance, Europe will continue to occupy the middle ground it already holds relative to Asia and North America. It promises no exceptional developments. Even the expected maintenance of its significant surplus of particle board and fibreboard will continue to be counterbalanced by plywood and veneer imports.

· Europe and North America, as well as Japan and China, the leading consumers in Asia, will continue to account for considerably more than three-quarters of industrial forest products. As these regions and countries are wholly or largely in the temperate and/or boreal zones, these forest ecosystems will continue to bear the main pressure for production.

· Actual production of industrial roundwood in South America is already quite significant, approaching one-tenth of the world total. Africa has very limited production at present. Both regions, however, have potential to increase supply of forest products from natural forests and, in the case of South America, from plantations. The principal bottlenecks relate to accessibility: first, due to infrastructural inadequacies in the main closed forest blocks; and second, due to public opinion barriers related to environmental concerns, especially for the rainforests of the Amazon and Zaire basins.

· Africa's largely rural population with low income creates special needs for fuelwood and non-wood forest products; African countries are faced with the need to support efforts to sustain supplies of these products even though they may not generate revenue. Competition for land with agriculture is an important factor in future resource provision strategies.

· Fuelwood consumption will remain dispersed throughout the developing world (with Asia leading) but the centre of gravity for industrial forest products will remain centred on the Pacific Basin. In many ways, North America and Asia will still serve as mirror images of each other - the former as supplier, the latter as a source of demand. The share of world consumption in 2010 for these two regions is expected to range from 56 percent for fuelwood to around 70 percent for all pulp and paper commodities. Major trade flows and supply alliances can be expected between Asia, Oceania and both Americas in the Pacific Rim and its Basin. Among these, a factor currently beyond assessment with any certainty, is the potentially large role that the Russian Far East and Siberian resource can play. South America is another area of promise whose possibilities have barely made themselves felt so far.

Table 3

World fuelwood and industrial roundwood consumption12

12 Brooks et al., op. cit., (footnote 8, page 76) Tables 2.1, 2.2, 3.3; FAO, op, cit, (footnote 1, page 74)

|

source |

projected world consumption (109 m3) |

|||

|

2000 |

2010 |

|||

|

quantity |

FAO's 1996 projection = 100 |

quantity |

FAO's 1996 projection = 100 |

|

|

fuelwood |

||||

|

FAO 1995 |

2.09 |

111 |

2.38 |

116 |

|

FAO 1996 provisional |

1.88 |

100 |

2.05 |

100 |

|

Apsey & Reed |

n.a. |

n.a. |

2.52 |

123 |

|

World Bank |

3.12 |

149 |

3.45 |

168 |

|

Zuidema (1994) |

n.a. |

n.a. |

1.50 |

73 |

|

Nilsson(1996) |

3.80 |

202 |

4.25 |

207 |

|

Brooks et al. constant 1990 per caput |

2.12 |

113 |

2.44 |

119 |

|

Brooks et al. lower GDP growth |

1.90 |

101 |

1.98 |

97 |

|

Brooks et al. higher GDP growth |

1.90 |

101 |

1.94 |

95 |

|

industrial roundwood |

||||

|

FAO 1995 |

1.90 |

117 |

2.28 |

128 |

|

FAO 1996 provisional |

1.63 |

100 |

1.78 |

100 |

|

Apsey & Reed |

1.79 |

110 |

1.94 |

109 |

|

Sedjo & Lyon (1995) |

1.81 |

111 |

1.97 |

111 |

|

Nilsson (1996) |

1.73 |

192 |

1.89 |

106 |

|

Simons (1994) |

n.a. |

n.a. |

2.15 |

120 |

|

Jaako Poyry (1995) |

1.50 |

92 |

1.70 |

96 |

|

Brooks et al. constant 1990 per caput |

1.89 |

116 |

2.03 |

114 |

|

Brooks et al. lower GDP scenario 1 - higher price increase |

1.73 |

106 |

1.84 |

103 |

|

Brooks et al. higher GDP scenario 2 - zero price increase |

1.81 |

111 |

2.09 |

117 |

|

Box 2 The second North American Timber Trends Study (NATTS)13, reported by Boulter and Darr, assessed timber demand and supply to 2015 for Canada and the USA which together account for about one-third of world industrial roundwood production. The study reports that during the last three decades North American timber harvests have increased quite dramatically but that North America will remain relatively self-contained for timber supply in future. 13 UN-ECE/FAO. 1996. North American Timber Trends Study. ECE/TIM/SP/9. Geneva. A key observation is that the region will, for the first time, face increasing timber demands without having a reserve of high-quality coniferous roundwood. This could cause a rise in prices for wood, and potential for greater substitution by non-wood materials. Future prospects for US timber supplies are affected largely by non-market forces; adoption of 'ecosystem management' and, in part, the application of the Endangered Species Act, have reduced annual timber from Federal lands from about 50 million m3 to less than 20 million m3. On private lands large diameter softwood timber will be nearly exhausted after year 2000 but by 2010 plantations will reach merchantable size in the South and the Pacific Northwest and will ensure adequate supplies in the long term. In the interim, the USA may need to resort to more intensive use of hardwoods and to imports. Consumer resistance by a market used to softwoods could be one problem; another would be how to adapt industrial infrastructure to a new raw material for what could be only a limited period before plantations offer adequate softwoods again. In Canada, future harvest trends suggest decline because: (a) 60 percent of the allowable annual harvest for industrial roundwood is hardwoods while most demand is for softwood; and (b) there is public pressure for more non-timber and environmental values especially since forests are largely old-growth natural forests. Canada still has, however, substantial stocks of mature and over-mature timber which can be harvested if the market will accept a significant switch from softwood. Technological improvements have so far minimized the increase in requirements for forest raw materials. US logging residues have decreased from 37 percent in 1962 to less than 10 percent of softwood growing stock volume at the logging site. In Canada, it takes only 1.98 m3 of roundwood to produce 1 m3 of lumber and plywood, down from 2.67 m3 in 1970. Significant advances in pulp and paper have occurred: in Canadian pulp manufacture, consumption of wood residues already surpassed that of roundwood in 1983; recycling of paper and paperboard has reached about 33 percent in the USA from 25 percent in 1988, and 12 percent of Canadian levels; and members of the American Forest and Paper Association have already met the 1995 goal of 40 percent recovery of paper and paperboard. There is only limited further opportunity for additional residue 'harvest' that could have a significant effect on the supply situation. Trade with other regions will continue. However, exports of coniferous logs to Pacific Rim markets, which reached over 20 million m3 in 1989, later declined to 10.9 million m3 in 1993. There is now a ban on exports of softwood logs from public lands in the western USA, and Canadian Provinces also have various restrictions. This trend may persist. There are no restrictions on exports of logs from private US lands and all current exports from the Western States of the US are from second-growth forests on private lands. |

|

Box 3 The outcome of the fifth European Timber Trends Study (ETTSV) has just been published with a year 2020 horizon.14 Two base scenarios were constructed, as well as a number of alternative scenarios to explore areas of uncertainty or policy choice: for BASE LOW, GDP growth till 2005 would average about 1.8 percent per annum and for BASE HIGH, 2.8 percent per annum. After 2005, GDP would grow at about 1.5 percent per annum for both scenarios. 14 European Timber Trends and Prospects: into the 21st Century. Doc: ECE/TIM/SP/11 Geneva Timber and Forest Study Papers. UN-ECE/FAO 1996. Roundwood harvest from European forests is expected to rise slowly. The area of Europe's 'exploitable' forest, of which the transition countries account for just over one-quarter (26 percent), is expected to grow by just under 5 million ha (about 3 percent) between 1990 and 2020 mostly with no increase in the Nordic countries, despite the availability of large areas of former agricultural land. ETTSV expects the demand for forest products to continue to grow, with further substitution possible among the various forest products. Long-term stability in prices was considered likely, although moderate price rises cannot be excluded. To help meet expanding needs, Europe's harvest is expected to increase by 23 percent to around 480 million m3 a year in 2020, with an estimated maximum in strong market conditions of 530 million m3. European forest industries production is projected to grow by 20-30 percent for sawnwood, 50-60 percent for wood based panels, 20-30 percent for pulp and around 65-85 percent for paper from the 1990 level. Projected removals in 2020 will be only 70 percent of the net annual increment and the share of European removals in the region's wood and fibre supply is expected to decline from two-thirds in 1990 to just over half in 2020. In the BASE LOW scenario, Europe's net imports of forest products (excluding roundwood) from other regions are expected to increase, particularly with regard to paper, by about 55 million m3 EQ (equivalent wood in the rough) and in the BASE HIGH about 80 million m3 EQ. In addition, imports of roundwood may increase by about 25 million m3 but this might be met from additional European supply, depending on delivered wood cost. While the share of net imports in fibre supply will rise, that of industrial wood residues will stay constant, and that of waste paper will rise steeply, to nearly one-fifth. The European transition countries are forecast to change from net exporters to net importers, because of stronger domestic demand and generally more prudent forest management policies. The reason for continued import of forest products from other regions, while Europe's own forests are under-harvested, rests strongly on the relative competitiveness of different wood sources; European producers are frequently at a disadvantage, because of high costs, fragmented ownership and other factors compared with other regions. About 49 percent of European consumption of paper and paperboard will be recovered for re-use in 2020 (i.e., excluding waste paper used as a source of energy) compared to 37 percent in 1990; in the transition countries the recovery rate is expected to rise from 31 percent to 36 percent. There will also be greater use of residues. About 75 percent of total residues produced will be used as raw material in 2010 (61 percent in 1990); much of the rest will be used for energy. |

Comparison with other projections

Since the release of the 1991 projections, FAO has successively reduced its estimates of global consumption except for 'other fibre pulp' (which has risen in the latest projections) on the basis of lowered assumed rates of economic growth that can be sustained for long periods.

Comparisons are possible with those studies which have similar commodity or regional coverage. Table 3 shows different projections, at world level, for fuelwood and industrial roundwood consumption from the studies mentioned in Box 1. Some differences in scope or definitions should be considered in making comparisons. For example, Nilsson seems to have dealt with 'basic requirements', which could be substantially different from the actual consumption projected by FAO. Zuidema's 1994 forecasts are of fuelwood 'availability' which is not necessarily the same as consumption.

At regional level, the salient points from the results of the North American Timber Trends Study (see Box 2) and the fifth European Timber Trends Study (see Box 3) are summarized. FAO is undertaking an in-depth outlook study for Asia (to be followed by other regions) which should shed more light on key potentials, opportunities and issues in all regions, including considerations relevant to the global situation.

Several elements of the projected developments have policy implications, which have been discussed briefly at the beginning of this section. The following elements can be highlighted:

· While the projections suggest a situation of no-crisis in terms of meeting demand, ensuring adequate supplies will require commitment to continued establishment of additional forest resources, and to extension of management to the large proportion of existing forests which are not managed at all.· The fact that the global picture may suggest no need for major concern should not divert attention from the urgent needs of many specific developing countries and locations where fuelwood is scarce. This commodity is not internationally tradable and countries lack adequate financial resources for improving the situation. Thus countries cannot solve their scarcity in any way except by establishing their own new resources and by containing demand.

· In the developed region of North America, potentially tight supplies of softwood offer an opportunity to broaden utilization to hardwoods. However, given that this is a temporary situation, adjustment of the industrial infrastructure to a different raw material may not prove viable. There may be opportunities for the export of hardwoods and the compensatory import of softwoods until enough North American softwood plantations mature.

· The possibility of wood supplies being adequate to meet future needs presupposes maintenance of balanced forest policies which allow continued industrial exploitation while environmental and recreation needs are also met. It will require moderation and self-restraint by society and its institutions at all levels to secure such balance. The potential of polarized positions to disrupt supplies exists in all regions whether industrialized or developing. For the tropics, campaigns in the consumer world that seek to bar improved access to major areas of forests are already in evidence; in industrialized countries, similar pressures could emerge with regard to remaining natural forests in North America and Siberia.

· North America, temperate Asia and Europe will remain dominant in the world forest products economy. Therefore, at a world level, most industrial utilization pressure will continue to be exerted largely on temperate/boreal forests. Given the increasing public concern at further erosion of biological diversity in these forests, action will be needed to ensure adoption of management practices that will continue to permit adequate timber yields while satisfying growing environmental objectives.

· The world forest products economy will be heavily dominated by two blocks on either side of the Pacific, i.e., North America and Asia. This development will, by placing all the countries that border on the Pacific on the front line of international trade, make it particularly important that open trading regimes are maintained among them to avoid dislocation of markets which could disturb forest industry patterns everywhere.

· The 'wild card' in all this is that of possible future developments in the former USSR. Russia in particular holds some of the world's largest potentially usable forests. It also spans the East and the West, being able, therefore, to influence events in both the Pacific Basin and in Western Europe. In broad terms, it is now supplying the West, alongside central European and Baltic countries, from west of the Urals. To the east of the Urals, transport and other problems have created a barrier with most of Siberia, but the Russian far east is accessible and is on the doorstep of both China and Japan - by far the largest consumer countries in Asia. Important questions are: how fast will the situation east of the Urals improve; will Russia export logs or increase industrial processing; if processing is carried out in a little-populated area such as Siberia, what will happen to the residues? These are some of the currently unanswerable questions regarding one of the largest potential supply sources.

· Developments in Japan could also have a decisive influence; Japan is one of the world's most highly-forested countries but has so far not harvested to any extent. Its forests are generally of small size and on difficult terrain. A policy and institutional change reflected in appropriate incentives could make industrial processing of this material possible but seems unlikely. However, if it did occur, it would affect the major trade flows since Japan is a leading importer from many countries.

Finally, policy must be concerned with sustainability: the findings of the outlook study suggest the need to contain demand within supply potentials. Improvement in management is clearly needed. Deforestation remains high in some regions, pollution damage in others. Erosion of biological richness may not be fully reversible in many boreal and temperate forests, but the situation can be improved. The relative importance given to wood supply or to other functions of forests will, however, need to reflect public, choice and societal values, and may therefore differ between and within regions or even countries. The outlook study makes reference to this but it is for policy-makers and society at large to make the necessary commitments to action, bearing in mind that preservation alone is no solution and that resource creation, while important, is no solution if not accompanied by responsible consumer behaviour. Policies concerned with consumer behaviour will, however, need to recognize that consumption levels are sometimes governed by necessity and cannot be easily modified.

Figures 1 to 11 on the following pages present a graphical summary of selected developments and prospects in production and international net trade.

Figure 2 - Production of industrial roundwood by region, 1990-2010

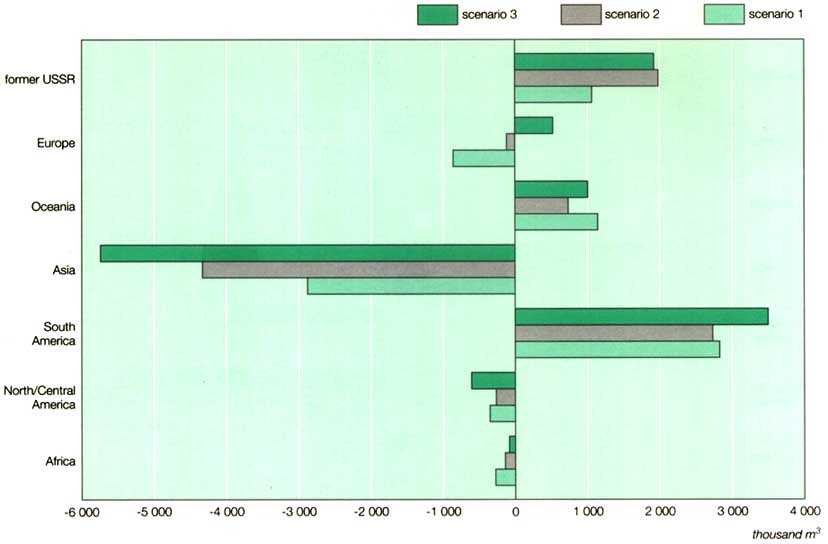

Figure 3 - Net trade in industrial roundwood in 201 015

15 Scenario 2 is the most probable (see text). Scenarios 1 and 3 differ in raw material and demand assumptions

Figure 4 - Production of sawnwood and sleepers by region, 1990-2010

Figure 5 - Net trade in sawnwood and sleepers in 201 016

16 Scenario 2 is the most probable (see text). Scenarios 1 and 3 differ in raw material and demand assumptions

Figure 6 - Production of wood-based panels by region, 1990-2010

Figure 7 - Net trade in wood-based panels in 201 017

17 Scenario 2 is the most probable (see text). Scenarios 1 and 3 differ in raw material and demand assumptions

Figure 8 - Production of paper and paperboard by region, 1990-2010

Figure 9 - Net trade in paper and paperboard in 201 018

18 Scenario 2 is the most probable (see text). Scenarios 1 and 3 differ in raw material and demand assumptions

Figure 10 - Production of total fibre furnish by region, 1990-2010

Figure 11 - Production of waste paper, 1965-2010

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}