Annual planning and budgeting

Sound results-based management (RBM) of an investment operation requires annual work plans (or operational plans) and budgets (AWPBs) to be well prepared and closely linked to a project’s results framework (RF) or logical framework (LF).

Experience has shown that adopting a results-based approach greatly enhances effectiveness and efficiency of investment project/programme/plan [later in the text referred to as ‘project’] implementation and increases the likelihood of achieving the stated objectives. This note provides an overview of concepts and issues related to AWPBs.

An AWPB is a project management tool. It is derived from a project’s overall work plan and budget (OWPB) which should be prepared prior to project start on the basis of the RF or LF (see: RBM). E.g., World Bank funded projects include an OWPB as part of the Project Implementation Plan. An AWPB is usually prepared by project component, structured to reflect outputs and allocating funds by activity.

The main features of AWPBs are: (i) clearly defined activities with targets linked to outputs for which indicators are defined that are also captured in the monitoring and evaluation (M&E) system (see: M&E); (ii) phasing of activities during the year (may be presented in a Gantt chart); (iii) specification of who is responsible for an activity (e.g. agency, unit or individual) and who are partners in implementation (if applicable); and (iv) a detailed breakdown of budget allocation by activity (which may be broken down into different inputs), including source of funding. The OWPB and AWPB also provide the basis for the procurement plan required to purchase and contract goods and services. It is important that the work plan and the budget are aligned, i.e. both are results-based. However, the use of special project costing software allows to present a results-based project budget, once prepared, also by other categories (e.g. expenditure, disbursement and procurement accounts), if required (see: Costing).

As for the RF/LF, the preparation of the first AWPB should involve all relevant stakeholders to ensure a common understanding of the project objectives, and its activities and annual budget allocation. It is also important that stakeholder involvement continues during the review of the AWPB at the end of the year and in the preparation of subsequent AWPBs. (see below and: Supervision and implementation support).

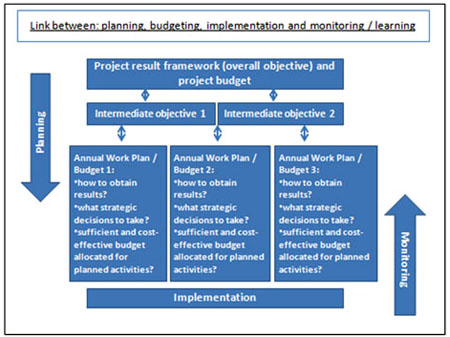

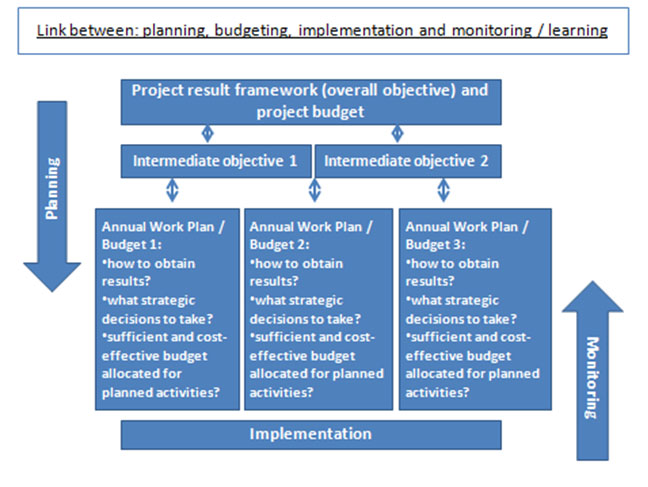

Planning, implementation, monitoring and budgetary responses are closely linked

Planning, budgeting and M&E are closely linked and are critical for managing and guiding efficient and effective design and implementation of investment projects in order to achieve the desired development results. Good planning and budgeting provides the basis for effective implementation and M&E. M&E can only be carried out and will be meaningful, if sufficiently detailed and results-oriented plans and budgets with clear objectives and targets exist. (see: M&E; RBM).

When preparing an AWPB it is good practice to divide the year into blocks of one or two months and to establish targets and budget needed for each of them. The use of quarterly targets is also an option but less precise because delays in implementation or budget shortfalls are not as promptly recognized. Although for some activities it may only be feasible to set targets and budgets on a quarterly, half-yearly or annual basis, reporting on achievements and disbursement can still take place on a monthly or bi-monthly basis.

For realistic budget planning, it is important to specify, to the extent possible, the unit, the unit costs and the number of units per planning period. For example, a unit could be one workshop, one farmer field school or one training day per participant. That way it will be easier, from year to year, to adjust unit costs if required and realistically plan the financial needs. As appropriate, activities may also be costed as lump sum or be broken down into items that are costed separately (see: Costing).

Annual reviews as well as participatory processes are necessary to understand progress constraints, bottlenecks and resource requirements. Once identified, shortcomings can be addressed in subsequent AWPBs through adequate resource allocation or/and a modification of activities. Reviews may also recommend some activities be dropped or new activities be added.

Consequently, at the end of the AWPB period, and before preparing the next AWPB, a participatory project progress review involving all relevant stakeholders should be conducted. This review will be based on the available monitoring data and should ideally include also participatory review and planning workshops with beneficiaries and implementing partners in order to: (a) allow these stakeholders to contribute to the review and subsequent planning process, and (b) address more qualitative aspects of project performance and related issues that may not be captured by the project’s M&E system. The main features of the progress review include, by activity and output: (i) quantification of achievement/disbursement during the planning period, and cumulative since project start, vis-à-vis the plan; (ii) identification of reasons for deviation (if any); (iii) review of assumptions and risks identified at the planning stage (if any) and adjustments (as appropriate); (iv) formulation of corrective measures required to bring project back on track (if required), including responsibilities. Corrective measures may include, as appropriate, e.g.: (a) modify activity (to make it more relevant); (b) change scope of activity (e.g. reduce targets); (c) change budget allocation (e.g. increase budget to respond to increased unit costs or increased scope); (d) change implementation arrangements for an activity (e.g. change responsibilities); (e) add a new activity (e.g. in case existing activities were not sufficient to reach the output to which they were to contribute); and/or (f) drop an activity (in case it is not relevant anymore or it may not be possible to implement it given the prevailing conditions). The findings of the progress review will inform the preparation of the following AWPB.

Experience shows that in addition to weak internal budget planning, external influences can also have a major impact on budget planning and hence on project implementation. Planning and budgeting cycles of governments have to be considered to avoid situations in which potential public funds (“counterpart” funds) are restricted or blocked due to a lack of foresight in project budget planning. Another budget-related challenge for project implementation is the scenario in which a government disburses fewer funds to the project than had been transferred to government accounts by the financier. In order to avoid these pitfalls, it is crucial for planning to closely match project budget needs with government budget approval and release cycles. A general awareness of national and local government budget processes and dynamics is important as is the close coordination with relevant units in the partner institutions.

- [Click to view larger image]

Ensuring the highest possible participation in the planning and budgeting process

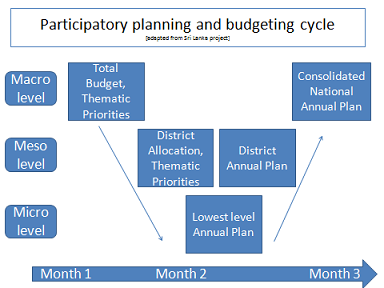

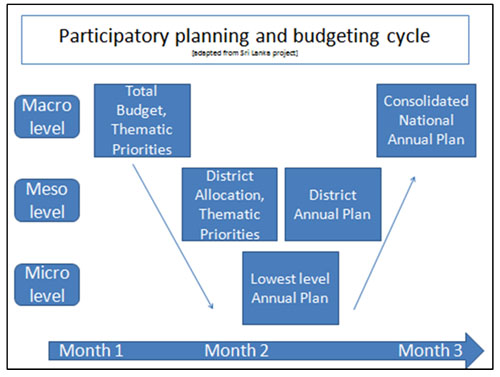

Following the principle of subsidiarity, participatory and inclusive preparation of AWPBs must ensure: (i) involvement of the most decentralized unit responsible for planning, implementation and achieving project targets (e.g. subnational level, territory entities, subproject); and (ii) good understanding of budget allocation processes at all relevant levels.

Usually, project teams or partners responsible for project implementation at the subnational level are most knowledgeable about implementation challenges and can therefore formulate realistic targets. Consequently, to the extent feasible, project units should be established at the most decentralized level, while timely and adequate funding needs to be ensured. Actually, in many cases the most decentralized unit only receives adequate financial support if the budget is coming directly from the next higher level.

Once the most decentralized unit to be involved has been identified, modalities for implementation need to be set up accordingly. For effective planning, budgeting and implementation of activities at field level, it is recommended that thematic guidance is provided from the meso level about the type of envisaged activities and corresponding budget envelope. To respond to eventual emergencies, or unexpected opportunities, all planning systems should entail a certain degree of flexibility.

At the end of each implementation cycle (e.g. after one year), an annual review of implementation progress and cost effectiveness should be conducted (see above). Findings should be made available to the implementation teams at all levels. Guidance and lessons learned should be incorporated into subsequent planning cycles. Monitoring the actual achievement and cost of implementing an activity or achieving an output (e.g. average cost of farm household/producer group supported, average cost per hectare provided with improved irrigation and drainage services) allows to measure project efficiency - in terms of (a) the actual project costs and duration for realizing the stated objectives, vis-à-vis the plan; and (b) the actual costs per unit of output (e.g. per producer group supported), vis-à-vis the planned costs per unit of output. This information will also provide an input into the Financial and Economic Analysis (FEA) which may be carried out during project implementation and in any case at project completion (see FEA).

Considering all of the above, it is good practice (with reference also to the Paris Declaration on Aid harmonization) to design investment projects that feed into and are aligned to the planning and budgeting mechanisms of existing national programmes and implementing departments. Although these national systems may at times have shortcomings, working through these systems contributes to building stronger locally owned systems. It is strongly advised not to create parallel project planning and budgeting systems, which will in any case terminate as soon as external funding has ended.

- [Click to view larger image]

Key Resources

Aid Delivery Methods - Project Cycle Management Guidelines (EU,2004) | An updated set of project design and management tools aimed at supporting good practices and decision-making throughout the project management cycle, so as to enhance relevance, feasibility and effectiveness of the programmes and projects supported with EC funds. |

Very focused resource providing DFID staff guidance on drafting Operational Plans as parts of planning across an organization below a central Business Plan. | |

Annual Work Plan Template - Format with monitoring component (UNDP, 2011) | Focused and practical resource by UNDP providing guidance and containing a template for preparing an Annual Work Plan. |

The resource consists of an Operating Expense Budget Planning model which is aimed to help managers in budgeting operating expenses, track actual expenses and estimate divergences between budgeted and real ones. | |